Insight Focus

Aluminium prices have surged on Middle East tensions. Higher prices could encourage exporters such as China to expand their global presence, although structural limits may cap gains. Brazil, despite its large production base, is expected to prioritise domestic supply amid tight market conditions and resource constraints.

As the conflict in the Middle East drags on with no clear resolution, major global players in the aluminium sector are reassessing their marketing strategies. Higher prices are expected to encourage increased exports from countries with spare capacity, such as China.

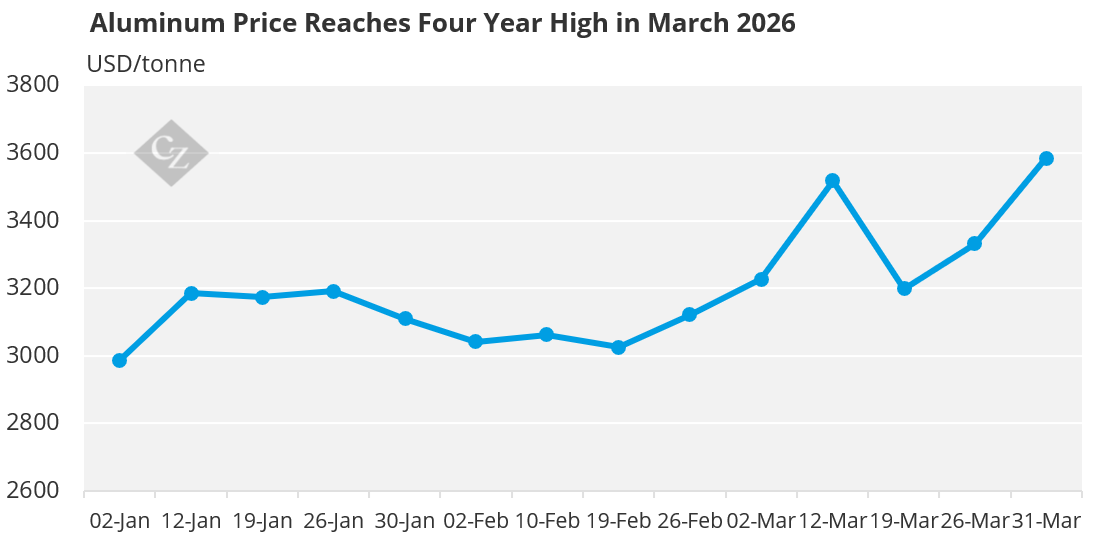

Aluminium prices have been hovering above USD 3,500/tonne, reaching their highest levels in four years. In March, the metal closed at USD 3,585/tonne on the London Metal Exchange (LME), up 17.3% from December last year.

Source: LME

China is set to expand its share of the global aluminium market as prices rise, although gains are likely to be constrained by restrictions such as the government’s 45 million-tonne annual production cap. The world’s largest producer is projected to increase exports by around 10% this year compared with 2025, according to consultancies including Wuchan Zhongda Futures and Aladdiny.

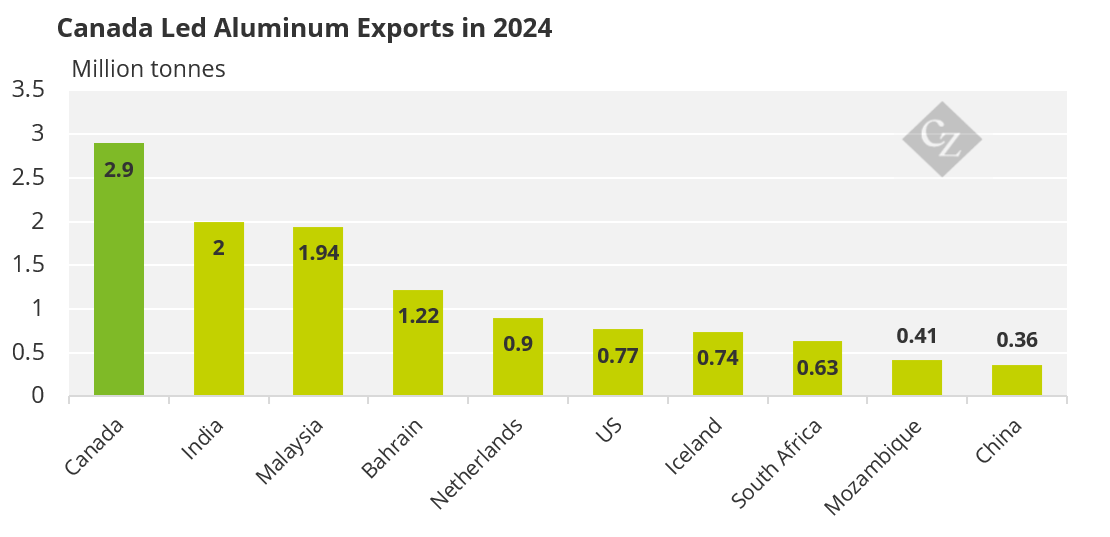

The additional volumes, however, are not expected to significantly increase global supply. China’s exports, at around 360,000 tonnes per year, are far below the levels achieved by countries such as Canada, India and Bahrain, which lead global shipments and are heavily affected by the war in the Persian Gulf.

Source: UN Comtrade

Brazil Protects Domestic Market

Brazil, one of the world’s largest producers of bauxite and primary aluminium, is set to focus its efforts on meeting domestic demand—for a clear reason. Domestic production capacity limits more significant advances in exports, especially in a scenario of instability in global production and trade chains.

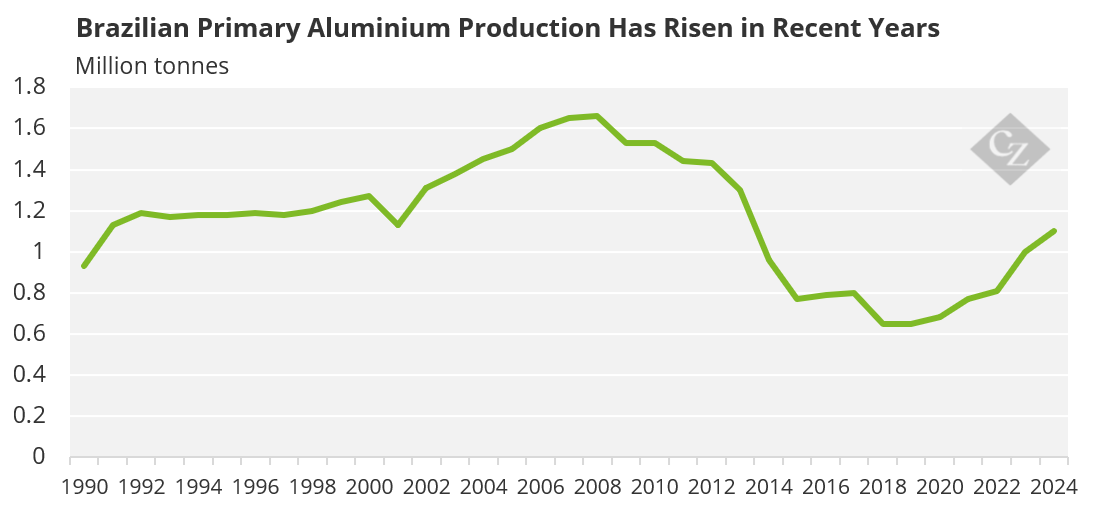

Currently, Brazil produces about 1.1 million tonnes of primary aluminium per year, a volume that is supplemented by approximately 1 million tonnes from recycled material. Domestic consumption, in turn, is around 1.9 million tonnes, according to the Brazilian Aluminium Association (ABAL), indicating a tight supply situation.

Although aluminium production has been growing in recent years, it remains far from the levels recorded in the 2000s, during the commodities boom, when strong demand from emerging countries drove up raw material prices.

Source: ABAL.

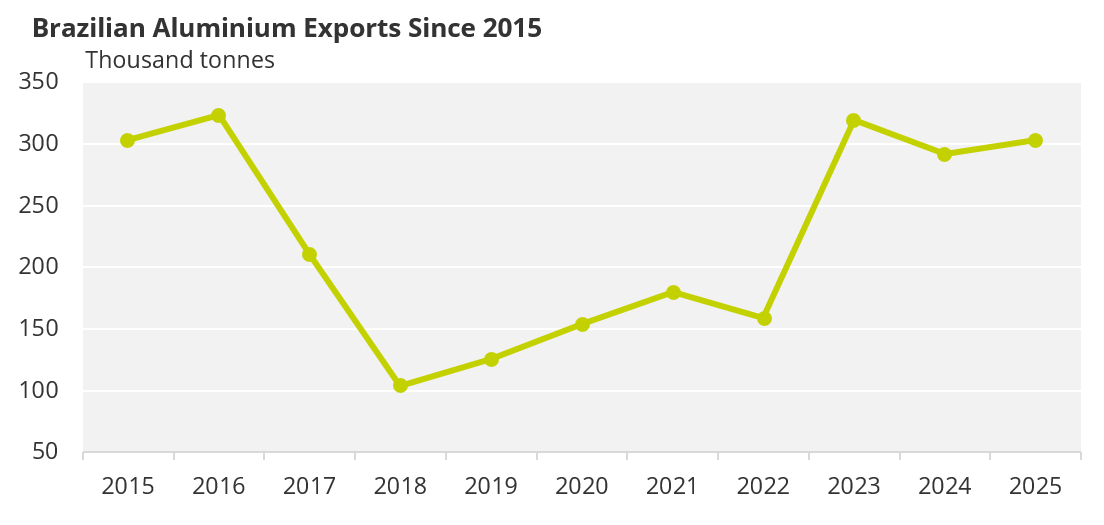

Aluminium exports, in turn, have followed variables such as the availability of aluminium in the domestic market, the cost of energy and domestic demand.

Source: Comex

“In a context of high volatility in the international market—which tends to intensify global competition for the metal—our biggest concern is not increasing exports, but rather ensuring the security of metal supply in the domestic market,” says Janaina Donas, CEO of ABAL, in an interview with CZ App.

Janaina Donas, Photo Courtesy of ABAL

Can Brazil scale up aluminium production and expand exports to capitalise on elevated global prices?

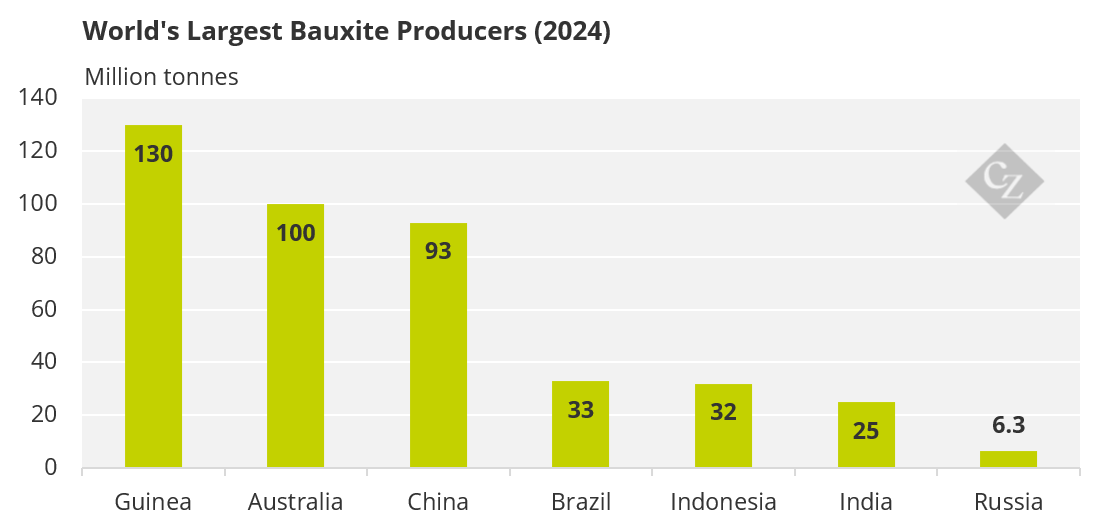

Brazil does indeed have the structural conditions for this. The country possesses a series of strategic assets that ensure the fulfillment of domestic demand and the country’s positioning in the global supply chain. Brazil is the world’s fourth largest producer of bauxite and the third largest producer of alumina. We have a vertically integrated chain, from mine to the finished product, which is a rare competitive advantage in the global scenario.

Source: US Geological Survey

Furthermore, Brazil’s rates of recycled aluminium use are among the highest in the world. Approximately 60% of aluminium product consumption in Brazil already comes from recycling, while the global average is around 28%.

Reactivating some previously reduced capacity could increase primary production to 1.3 million tonnes per year. Combined with secondary production from recycling, this would make Brazil self-sufficient in its metal supply. However, to go beyond this and significantly expand capacity, new investments in smelters are necessary, either through the expansion of existing plants or the construction of new units.

Aluminium ingots. Photo Courtesy of ABAL

And here is the crux of the matter: these projects have a long maturation horizon. Even for projects already in an advanced planning stage, the implementation time is about five years.

Investments of this magnitude depend on competitive energy costs, legal certainty, regulatory predictability and a stable business environment. These are long-term strategic decisions that companies make based on perspectives that go far beyond a geopolitical conflict.

And the majority of Brazil’s production serves the domestic market, correct?

Yes. Brazil consumes approximately 1.88 million tonnes of processed aluminium products per year, and current primary production of 1.1 million tonnes is still insufficient to meet this demand on its own. Self-sufficiency is only maintained when secondary production from our recycling chain—one of the most significant in the world—is included.

Therefore, in the context of high volatility in the international market, which tends to intensify global competition for the metal from both primary and secondary sources, our greatest concern at the moment is not increasing exports. It is ensuring the security of metal supply for the domestic market and strengthening the competitive advantages that allow us to maintain this self-sufficiency.

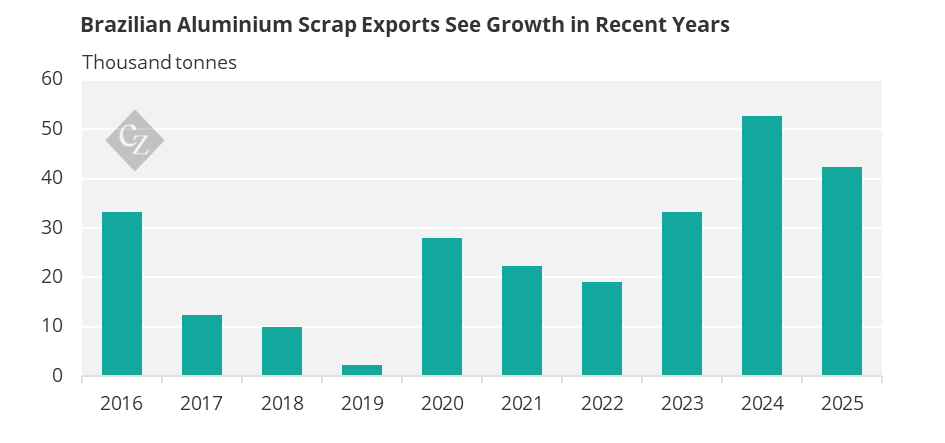

This is especially relevant because Brazil already faces a concrete problem in this regard: exports of aluminium scrap grew by 177% between 2022 and 2024, mainly destined for Asia.

Source: Comex.

This resulted in a deficit of approximately 100,000 tonnes of scrap metal in the domestic market between 2023 and 2024. While the world is trying to stock up on aluminium, we are exporting a strategic input that is lacking domestically. This is one of our priority areas for action.

That said, it is true that the instability in the Middle East puts Brazil on the radar of markets that historically depended on aluminium from the region. There is a concrete movement from the US signaling interest in partnerships around strategic minerals, and supposedly aluminium could be part of this agenda, just as it is already included in the lists of critical materials of the EU, Canada, the UK and Australia.

Aluminium sheets. Photo Courtesy of ABAL

However, the current signals point more towards products at the base of the supply chain than towards primary aluminium or manufactured goods with higher added value.

And this is the key point: Brazil cannot be content with being only a supplier of raw materials, especially at a time when the world most needs finished products. The difference in added value along the chain is substantial, with implications for jobs, income and regional development. The priority, before thinking about exporting more, is to ensure that we have enough metal to supply our market.