This update is from Sosland Publishing Co.’s weekly Sweetener Report. This update is from Sosland Publishing’s Sweetener Report. For more information and subscription details, CLICK HERE.

Insight Focus

- US beets look to be in decent good condition at this stage of their growth.

- Worries about slower sugar deliveries persist.

- The cash sugar market remains quiet.

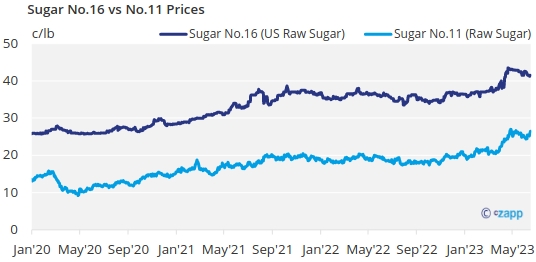

The cash sugar market was quiet amid slow spot and forward sales during the week ended June 16. Prices were unchanged, but a softer tone was expected to develop in spot values due to indications of slow deliveries of contract supplies to some buyers.

Beet crops were planted and emerged. The Colorado crop was too wet. The Michigan crop was too dry but received a needed shot of rain in the past couple of weeks. Crops in most other states were doing well with good-to-excellent ratings of 80% or above as of June 11, according to US Department of Agriculture state office reports. The Louisiana sugar cane crop had a good-to-excellent rating of 80%, slightly below last year’s 82% but still the second highest in the past decade.

Beet and cane crops now were at the mercy of the summer growing season. In areas where beets were planted later than desired, timely rainfall, plenty of heating degree days and no early frost are needed to maximize production. Sugar from early harvest counted in the current marketing year likely will be lower than last year.

Offers for bulk refined sugar for 2023-24 were unchanged from a week earlier. It was expected some price weakness could surface around October once harvest is fully underway and processors have a good idea of what their 2023-24 sugar production will be. It’s not uncommon for a brief period of price weakness at that time as processors sell most of their remaining supply (with which they are comfortable). Since several beet processors stopped selling sugar earlier this year, there may be more supply than usual available in October.

The spot market situation continues to develop amid ongoing slow deliveries of sugar reported by sellers. Ideas are that buyers are not taking all of their contracted sugar due to slow sales of manufactured food products. Slower deliveries to foodservice also were noted. Retail movement appears to be about as expected. As a result, a bit more bulk refined sugar is becoming available on the spot market. Also adding to supply were imports of high-duty sugar at prices below current offers for refined cane sugar in some areas. Spot list prices have not been lowered to date. Some expect minor price weakness to develop, although slower imports from Mexico (which are mostly raws) may impact the overall supply picture through the summer months.

The USDA in its June 9 supply-and-demand report left unchanged from May its 2022-23 forecast for deliveries of sugar for human consumption in the United States at 12,675,000 tons, up 1.6% from 2021-22. Most in the trade think that is too high considering deliveries through April were up only 0.8%, and it would be difficult to make up the difference in the last five months of the marketing year.

Distributors continued to note slow deliveries of 42% high-fructose corn syrup and of dextrose to buyers, allowing for supplies to be offered on the spot market at prices equivalent to 2023 annual contracted prices.