This update is from Sosland Publishing Co.’s weekly Sweetener Report. This update is from Sosland Publishing’s Sweetener Report. For more information and subscription details, CLICK HERE.

Insight Focus

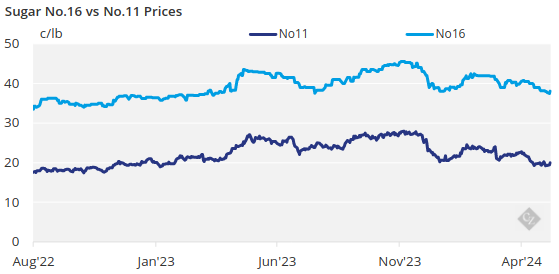

Active sugar beet planting in the key Red River Valley took centre stage in the sugar market during the week ended May 3. Spot prices were steady. Forward prices were unchanged but with a weak tone amid slow sales.

Prices Remain Unchanged

Spot prices were unchanged this week. At least one processor had withdrawn from the spot market, choosing to focus on new crop sales only. Beet sugar prices for the remainder of 2023-24 were offered at 55¢/lb to 58¢/lb FOB Midwest. Refined cane sugar for 2024 was offered at 62¢/lb FOB Northeast and West Coast and at 58¢/lb to 60¢/lb FOB Southeast and Gulf.

Bulk refined beet sugar for 2024-25 was said to be trading in the low 50¢/lb FOB area in the Midwest with indications of some activity below 50¢/lb to secure volume. Bulk refined cane sugar for 2025 was offered at 60¢/lb FOB Northeast and West Coast and 56¢/lb to 58¢/lb FOB Southeast and Gulf.

Planting Races Ahead

Favourable weather spurred planting progress to 66% complete in the four largest beet producing states as of April 28, jumping from 26% a week earlier and sharply higher than 22% a year ago. However, it was behind the 2019-23 average of 32%, the USDA said.

Planting soared to 81% in Minnesota — well above the average of 18% — and to 50% in North Dakota, exceeding the average of 10%. However, planting lagged in Idaho at 63% versus the 82% average and in Michigan at 49%, slightly behind the 52% average.

The speedy tempo in sugar beet planting weighed on values for next year that were already feeling pressure from the slow booking pace for new crop supplies. Some sellers expressed concerns about demand as high interest rates continued to impact their customers’ supply management strategies. Many buyers may be shifting to a hand-to-mouth buying approach to limit overly full inventories and maximize cash flow and opportunity costs.

“Our bookings have definitely slowed compared to the last couple of years, but that’s not a bad thing because we want our customers to really understand what their needs are,” one seller said.

Sellers Look to 2025 Sales

Most beet processors remained in the market for both 2023-24 and 2024-25. One processor was withholding additional 2025 sales until September when a better understanding of new crop supplies is known. However, he was still fulfilling spot requests for limited volumes.

For sugar buyers seeking to secure their 2024-25 coverage, traders said there may be opportunities to lock in a slight year-over-year discount. While some larger users were putting coverage on for 2025, most buyers seemed content to wait. Unlike recent years, domestic supply availability appeared less of a concern for next year. Sugar users’ lagging demand this year may be driving a more disciplined approach to buying for next year as they relinquish supply concerns instilled during the COVID pandemic.

Some inquiries about contracting and pricing for 2025 corn sweeteners surfaced, although it was expected no deals (other than tolling agreements) would be signed until August or September.