Insight Focus

- Raw and refined sugar speculators retreat back towards neutrality.

- Consumers continue to aggressively buy into No.11 weakness.

- The white premium has slowly recovered back to the 100USD/mt threshold.

New York No.11 (Raw Sugar)

The Mar’23 No.11 contract closed above 18.7c/lb by Friday last week, an upwards move of 1c/lb from the same period the week before. With the latest CoT data current to only the 1st of November, this rise be reflected in next week’s report.

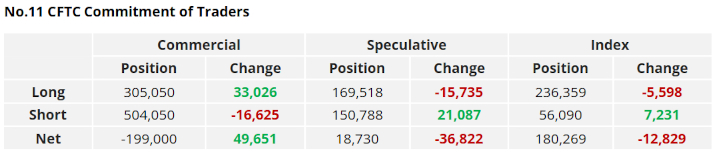

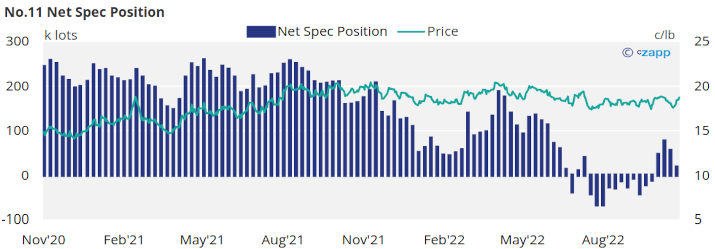

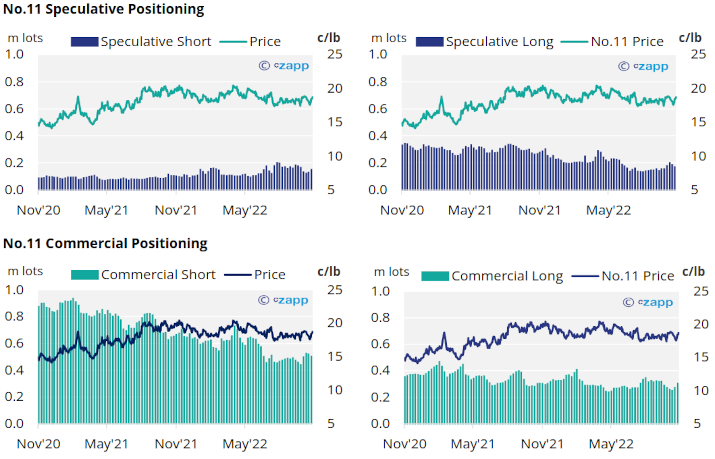

With the market instead much lower in the week to the 1st of November, raw sugar consumers continued to buy into weakness, adding over 33k lots of new hedges.

Producers were not willing to sell at this level, instead allowing 17k lots to close out. In recent months we have observed greater producer hedging with the market close to 19c/lb instead.

With the No.11 sinking as low as 17.7c/lb in the week to November 1st many more recent spec long positions have been closed.

In conjunction, with the opening of 21k new short positions the net spec position has retreated back towards neutrality, now under 20k lots long.

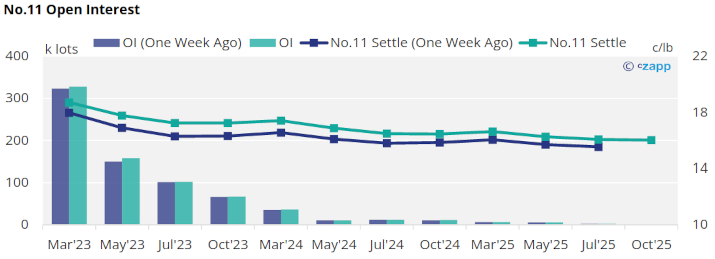

The No.11 forward curve is still backwardated to the middle of next before moving into contango into Mar’24, suggesting potential tightness in the market toward the end of 2023.

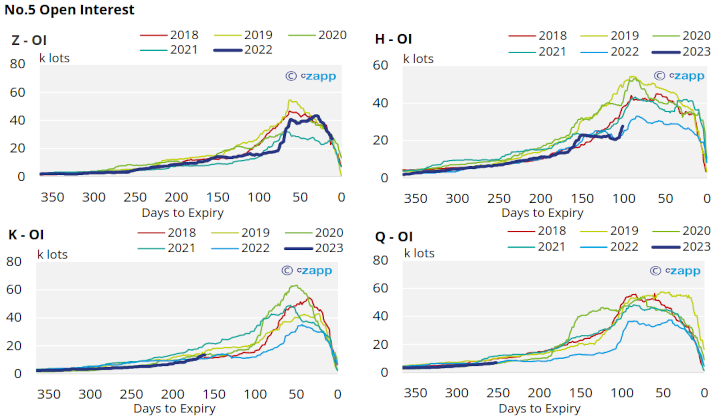

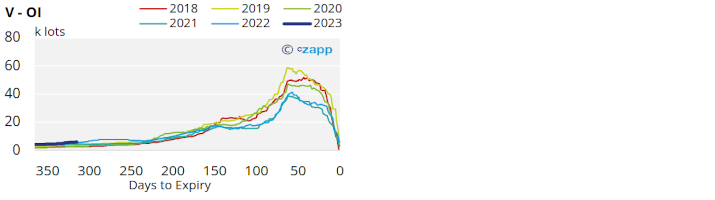

London No.5 (Refined Sugar)

No.5 refined sugar prices have also recovered over the last week, with the Dec’22 contract adding almost 20USD to reach 539USD/mt by Friday.

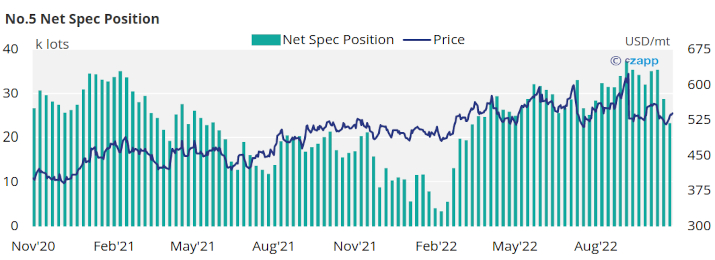

By the 1st of November with prices in decline, refined sugar speculators continue to aggressively lift their long held bullish view of the No.5 as another 5k lots of long positions are closed out.

This leaves the net spec position at its lowest level since March.

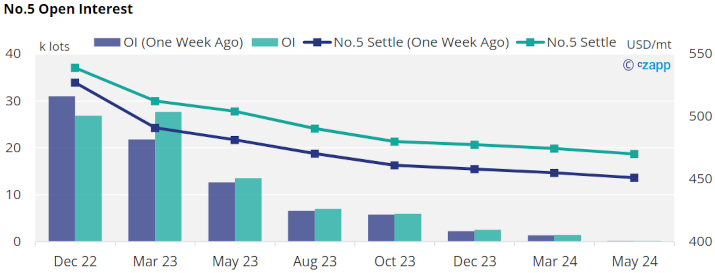

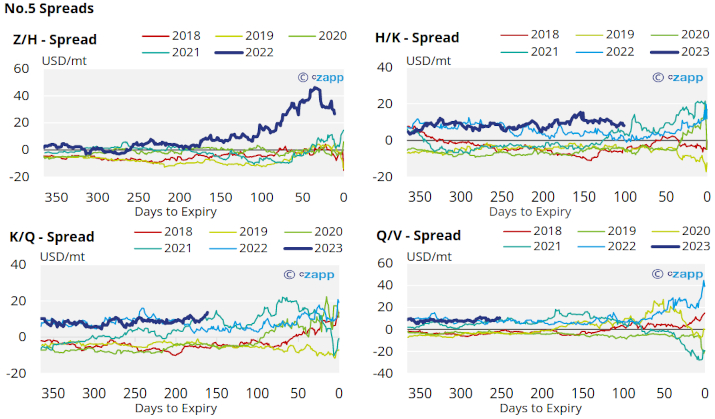

Z/H spreads have narrowed again to almost 25USD/mt premium as the Dec’22 contract draws close to expiry. Despite this the No.5 forward curve remains strongly inverted for all currently active contracts.

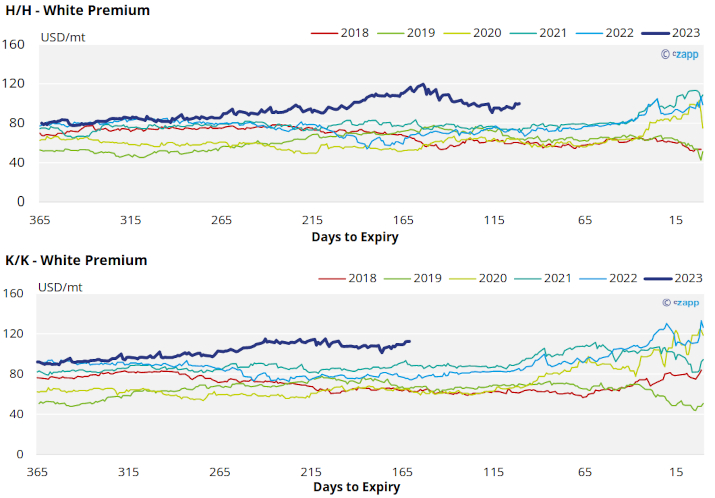

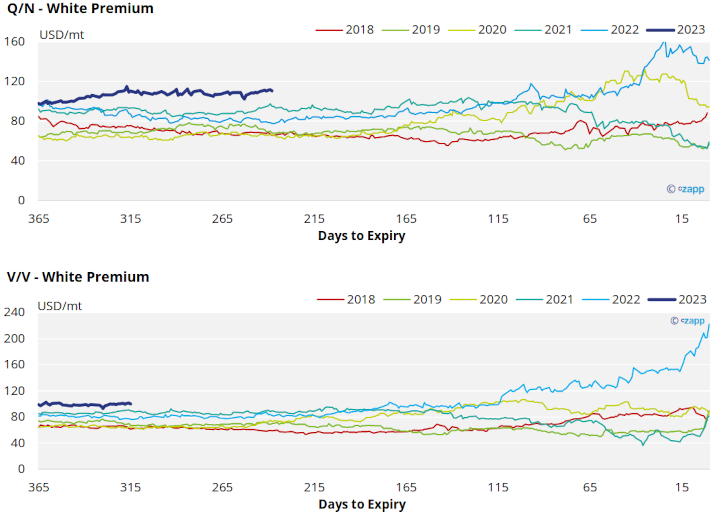

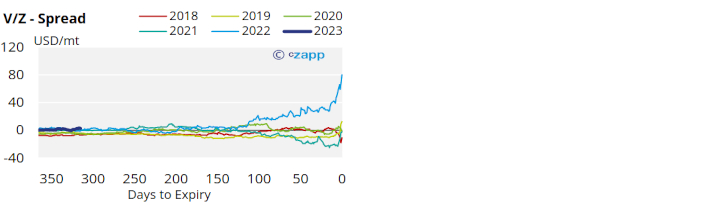

White Premium (Arbitrage)

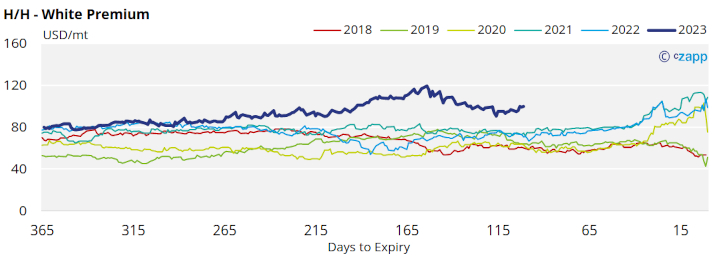

The sugar white premium continues its recovery, reaching almost 100USD/mt by Friday.

Whilst we think the wider white premium decline has been partially driven by bearish macroeconomic factors, there is also a growing case that inflationary pressure on economies around the world could be causing a decline in usually robust sugar demand.

Many re-exports refiners need around 120-130USD/mt above the No.11 to produce refined sugar, therefore the current white premium is not strong enough to incentivise this.

The proceeding K/K and Q/N white premiums remain above 100USD/mt, stronger than the front month H/H white premium, though this would still not be high enough to incentive strong re-export refining.

For a more detailed view of the sugar futures and market data, please refer to the data appendix below.

No.11 (Raw Sugar) Appendix

No.5 (White Sugar) Appendix

White Premium Appendix