What Is Corn Ethanol?

Corn ethanol is a renewable biofuel produced by fermenting and distilling the starch contained in corn kernels. While the US is the world’s largest producer, corn‑based ethanol contributes significantly to global biofuel use as countries expand renewable energy mandates to reduce dependence on fossil fuels.

Source: OECD

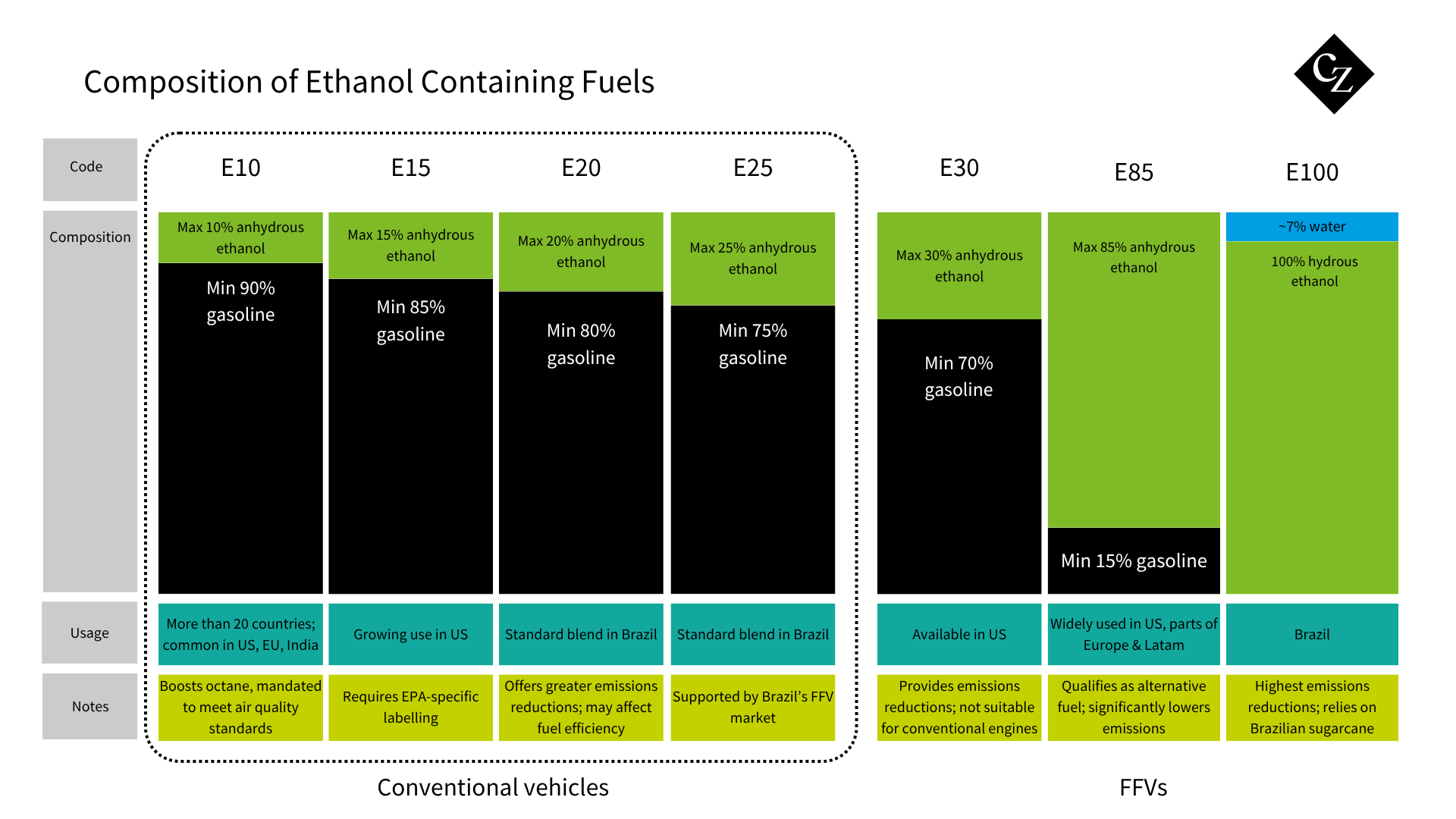

Ethanol is commonly blended with gasoline at various ratios—E10 (10% ethanol), E20 (20%), and higher blends are used across Latin America and parts of Asia.

In global energy systems, ethanol is valued for its ability to reduce greenhouse gas emissions, increase octane levels in gasoline and support agricultural economies. The Renewable Fuels Association highlights ethanol’s broad environmental and economic advantages, which have driven widespread international adoption of ethanol‑blending mandates.

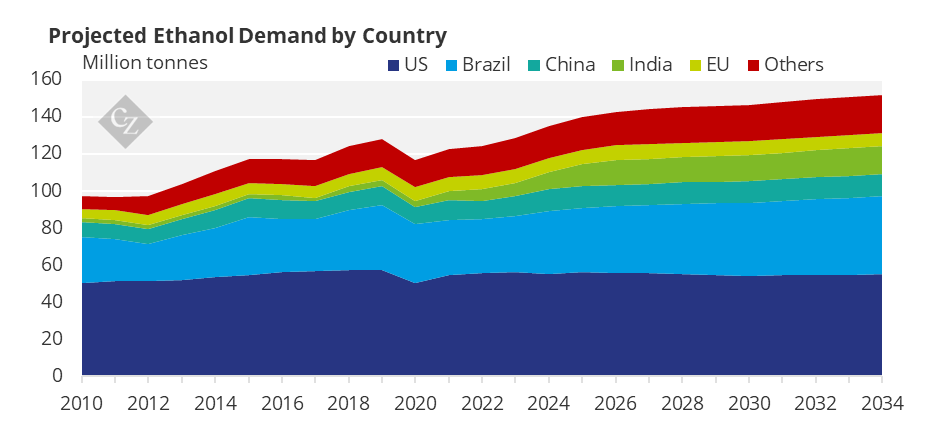

Though the US dominates corn ethanol production, other countries—including Brazil, China, India and several Southeast Asian nations—use corn and other feedstocks such as sugarcane, cassava and sorghum in their ethanol sectors. This diverse feedstock base reflects regional agricultural strengths and contributes to the global importance of ethanol as a transport fuel.

Source: RFA

Types of Ethanol Fuel Blends

Ethanol‑gasoline blends are typically designated with an “E‑number,” which represents the percentage of ethanol by volume in the fuel mixture. Globally, different countries adopt blends based on policy goals, engine compatibility, emissions-reduction strategies and agricultural capacity.

E10 (10% Ethanol, 90% Gasoline)

E10 is among the most widely used blends worldwide and is common in the US, Europe, India and Japan. It is approved for use in all modern gasoline vehicles without modification. E10 offers modest emissions benefits and helps countries meet air-quality and renewable-fuel mandates. In the US, E10 uptake accelerated under the Clean Air Act Amendments, and today most gasoline contains up to 10% ethanol.

E15 (10.5–15% Ethanol)

E15 is approved for model year 2001 and newer vehicles in the US and is increasingly adopted as a cost‑saving, lower-emissions option. Regulations require labelling and misfuelling mitigation measures to ensure older vehicles do not use E15. While not yet universally adopted globally, the blend is expanding, supported by cost benefits and renewable‑fuel policies.

E20 (20% Ethanol)

E20 is gaining global momentum. Brazil has used blends between E20 and E25 for decades, supported by widespread flex‑fuel vehicle adoption. India is rapidly expanding E20 availability, aiming for widespread use by 2025 as part of its broader energy‑security and decarbonization strategy. Japan has also announced action plans for adoption of E10 and E20, reflecting broader international support for higher ethanol blends.

E25 and E30 (25–30% Ethanol)

Intermediate blends such as E25 and E30 are used primarily in flexible‑fuel vehicles (FFVs), which are designed to run on higher ethanol concentrations. Brazil commonly uses E25 as its national standard blend, while blender pumps in the US provide E25 and E30 options for FFV drivers. These blends offer greater emissions reductions but require engines compatible with higher ethanol levels.

E85 (51–83% Ethanol)

E85 is a high‑ethanol blend used exclusively in flexible‑fuel vehicles. Ethanol content varies seasonally and by geography to ensure cold‑weather performance. E85 qualifies as an alternative fuel and significantly reduces lifecycle emissions compared with gasoline. The blend is widely available in the US and parts of Europe and Latin America.

E100 (100% Ethanol)

Used predominantly in Brazil, E100 (neat hydrous ethanol) powers vehicles specifically designed for pure ethanol or flex‑fuel systems. Brazil’s ethanol industry—built on sugarcane—has enabled mass adoption of E100 since the 1970s. Some countries, including the Netherlands, use specialised hydrous blends (e.g., hE15) in modern vehicles, though this remains less common globally.

Corn Ethanol Production Processes

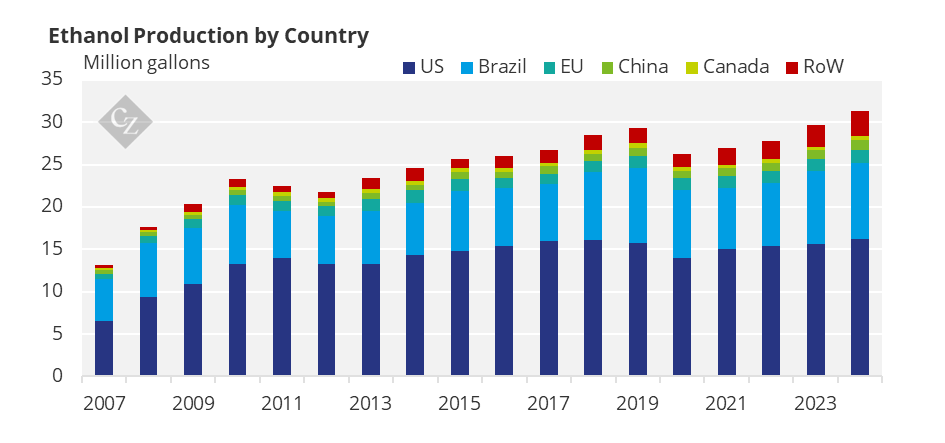

Globally, ethanol production uses two major pathways: starch‑based ethanol (from corn, wheat, and cassava) and sugar‑based ethanol (primarily sugarcane). Corn ethanol production is most concentrated in North America and parts of Asia, where corn availability is high.

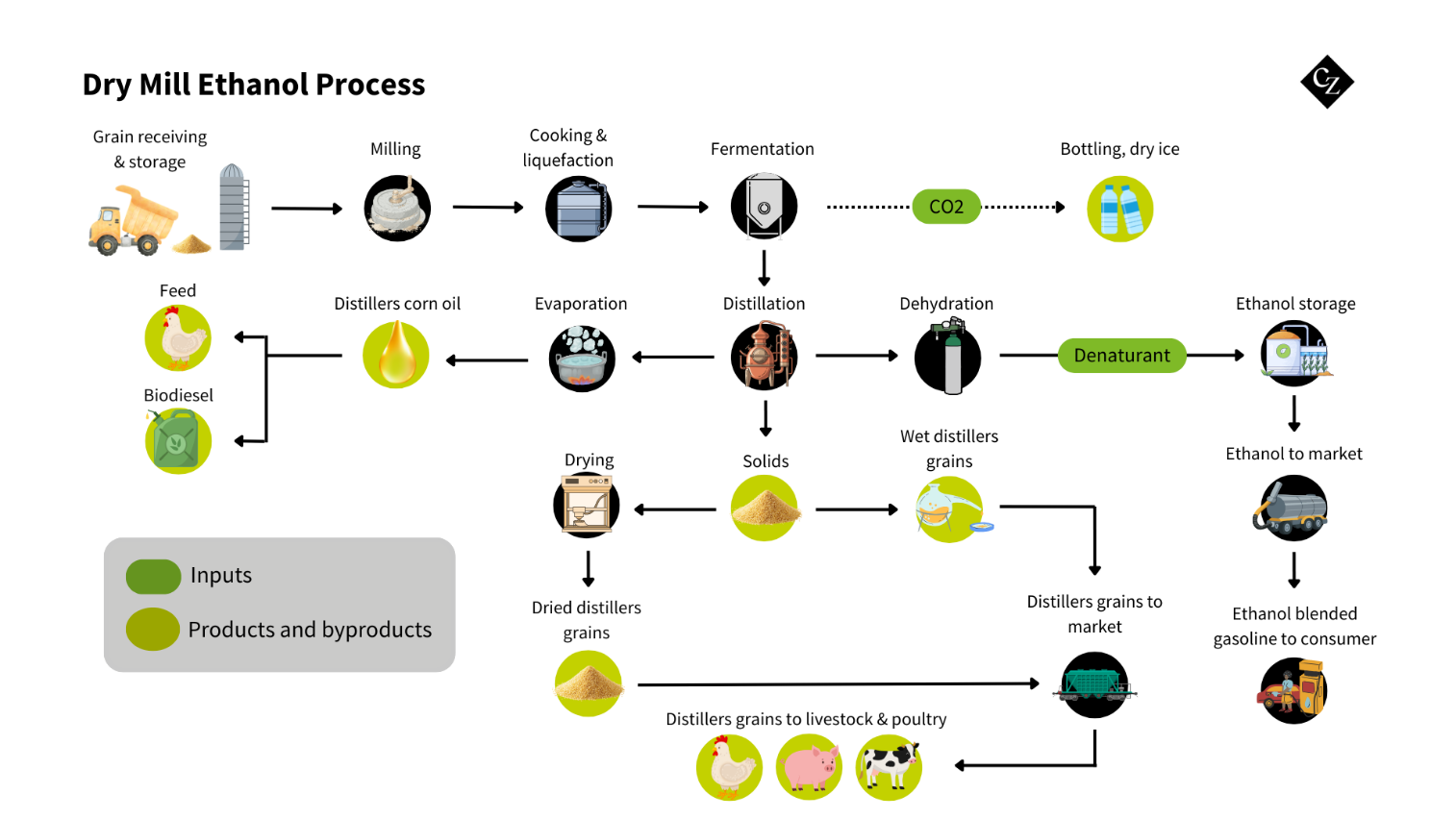

Nearly all US facilities—representing over half of global corn ethanol output—use the dry‑mill process. This process involves milling, cooking, enzymatic breakdown of starch, fermentation, distillation, and dehydration.

As of 2024, US refineries alone exceed 18 billion gallons of annual capacity, with facilities averaging 92 million gallons per year. While this scale is unmatched, other regions are expanding production capacity. For example:

-

Brazil, though known primarily for sugarcane ethanol, has expanded its corn ethanol footprint, particularly in the country’s interior, where corn surpluses support new biorefineries.

-

China, the world’s second‑largest corn producer, has periodically increased corn‑based ethanol output in response to stockpiles and clean‑energy goals.

-

India and Southeast Asia are exploring corn and blended-feedstock ethanol to supplement domestic energy strategies, aided by tariff adjustments and blending mandates.

Source: USDA

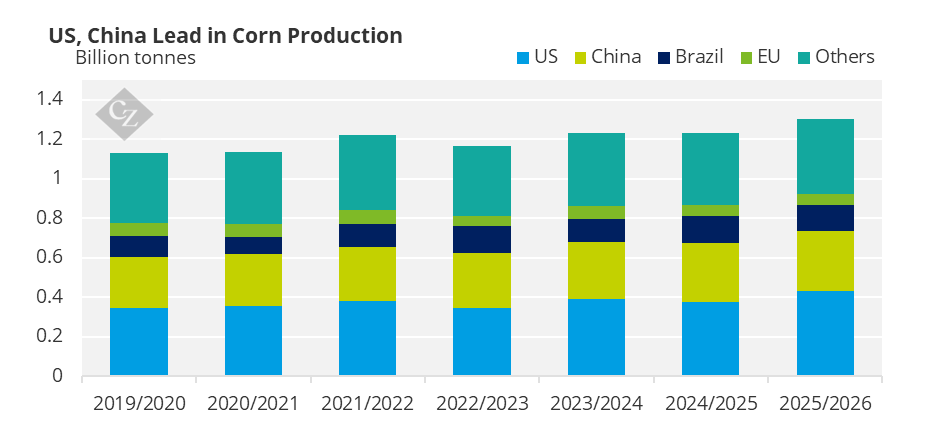

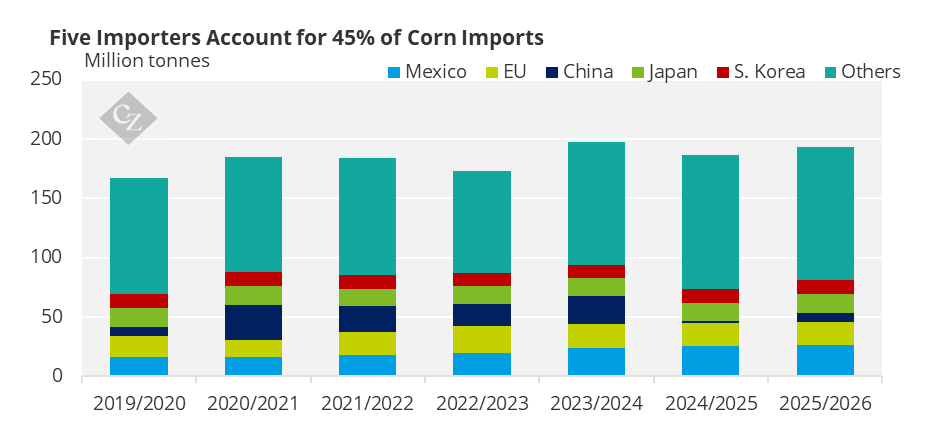

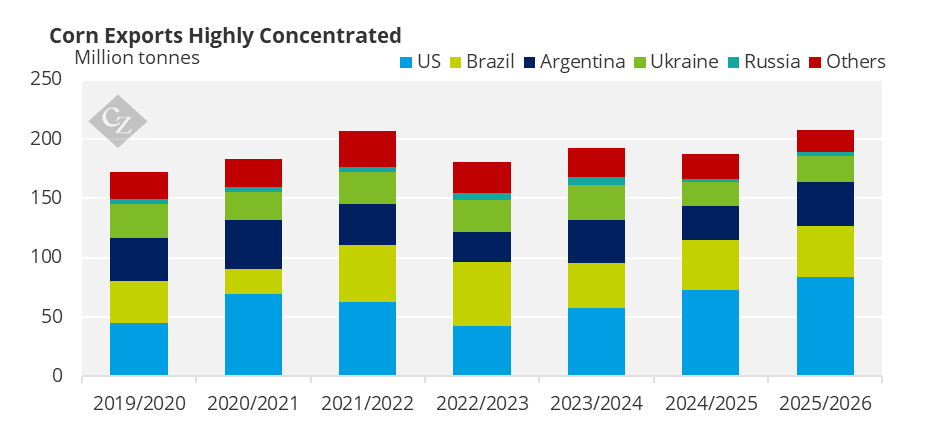

Corn Ethanol Import and Export in Global Markets

Ethanol is a globally traded commodity, with the US and Brazil accounting for most exports. Several regions are increasing imports to meet renewable fuel goals, stabilise domestic supply or diversify energy sources.

Source: USDA

Because corn availability influences ethanol production costs worldwide, changes in global corn trade indirectly shape ethanol trade patterns. For instance, higher corn exports alter feedstock availability for domestic ethanol industries, ultimately influencing import and export volumes of the finished fuel.

Global Corn Ethanol Pricing Dynamics

Corn ethanol pricing worldwide is shaped by several interconnected factors: feedstock markets, energy prices, domestic blending mandates, and global trade flows.

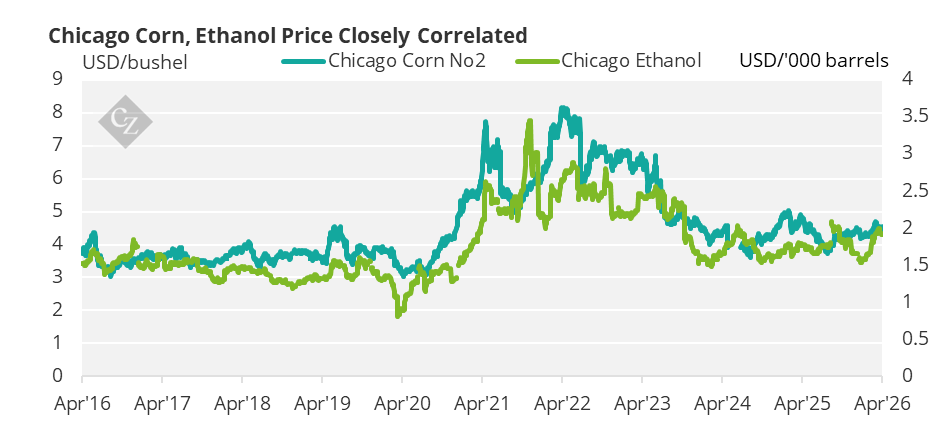

Feedstock and Commodity Market Links

Corn and ethanol futures show a strong positive correlation, with a long‑term coefficient of 0.83 between 2014 and 2024. Since corn is the dominant feedstock for ethanol in major producing regions, fluctuations in global corn supply, driven by weather conditions, geopolitical shifts, and changes in planted acreage, directly influence ethanol production costs.

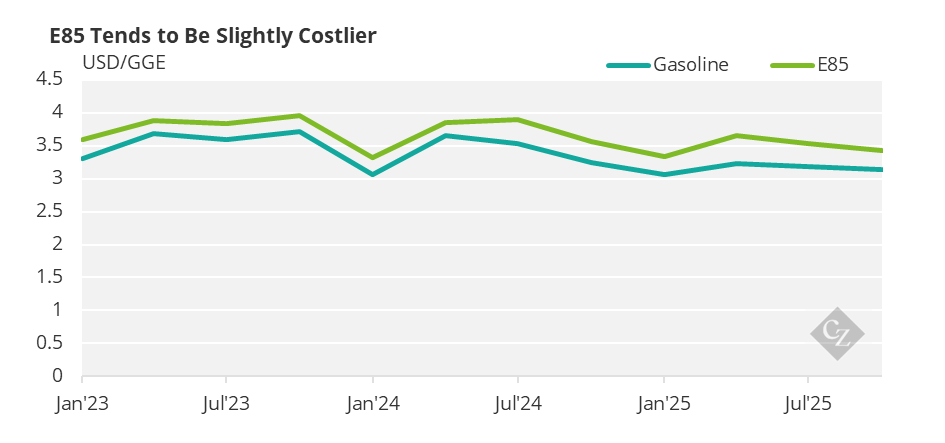

On the consumer side, higher ethanol blends can reduce costs per gallon. However, when adjusted for fuel efficiency E85 tends to be slightly more expensive.

Source: Alternative Fuels Data Center

However, price dynamics vary significantly by region:

-

US: Ethanol prices fell to an annual average of USD 1.60/gallon in 2024, down 25.7% from 2023, driven by lower feedstock costs and shifts in domestic demand.

-

Brazil: Ethanol pricing moves with sugar markets—producers dynamically adjust between sugar and ethanol depending on relative profitability.

-

Europe: EU demand is shaped by climate‑policy directives, which recently updated sustainability rules governing US corn ethanol imports.

-

Asia: Pricing is influenced by fuel‑import dependence, government incentives and domestic agricultural capacity. Tariff adjustments such as Vietnam lowering its ethanol duty from 15% to 10% reflect an effort to stabilize domestic fuel prices.

Globally, ethanol demand is strongly policy‑driven. Many countries maintain or are adopting E10 or higher blends, including Panama (E10 by 2026) and Colombia (restoration of E10 in 2024). Such mandates create stable demand conditions that influence long‑term pricing.

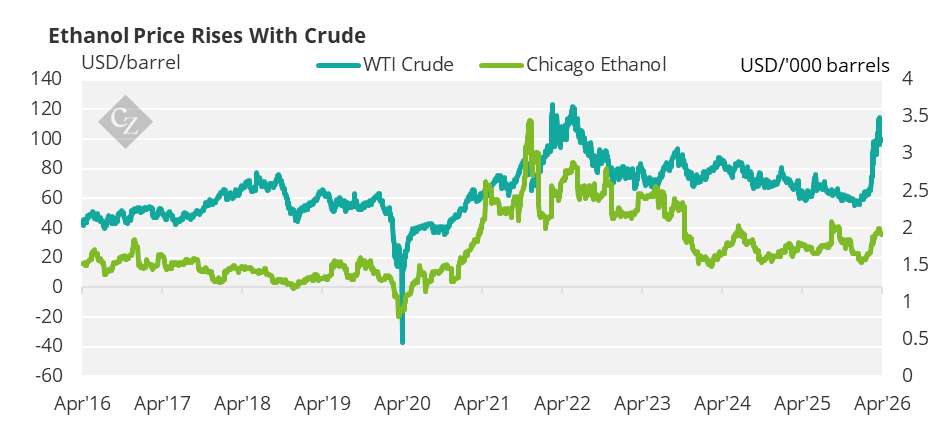

Corn Ethanol Pricing vs. Oil Prices

Corn ethanol pricing is shaped by a mix of agricultural, energy‑market and policy‑driven forces. While ethanol and crude oil operate in distinct commodity markets, their price trajectories frequently intersect, largely because ethanol competes directly with gasoline as a transportation fuel. Several key dynamics explain how and why corn ethanol prices respond to oil price movements.

1. Oil Prices Influence Gasoline Prices—and Therefore Ethanol Demand

Ethanol is primarily used as a gasoline blendstock, so when crude oil—and by extension, gasoline—prices rise, ethanol becomes a more economically attractive component of the fuel mix. Higher gasoline prices strengthen ethanol’s blend economics, boosting demand and supporting upward pressure on ethanol prices.

Source: EIA

Similarly, ethanol demand is closely tied to gasoline markets, with oil price fluctuations influencing consumer driving behaviour, fuel costs and competitive dynamics between fossil fuels and biofuels. When oil prices fall, gasoline becomes cheaper, reducing the relative economic incentive to use ethanol blends beyond mandated levels.

2. Corn Feedstock Costs Create Independent Volatility

Unlike petroleum fuels, ethanol prices are heavily dependent on agricultural inputs—especially corn. Corn price volatility driven by weather, crop yields, fertiliser costs and global trade affects ethanol production costs regardless of oil markets. Rising corn prices contributed materially to ethanol price increases in the US during 2025, independent of oil price movements.

The Agricultural Marketing Resource Center provides long‑run comparisons showing that crop prices and energy prices often move independently, contributing to highly variable ethanol profitability and periodic decoupling from oil‑price trends.

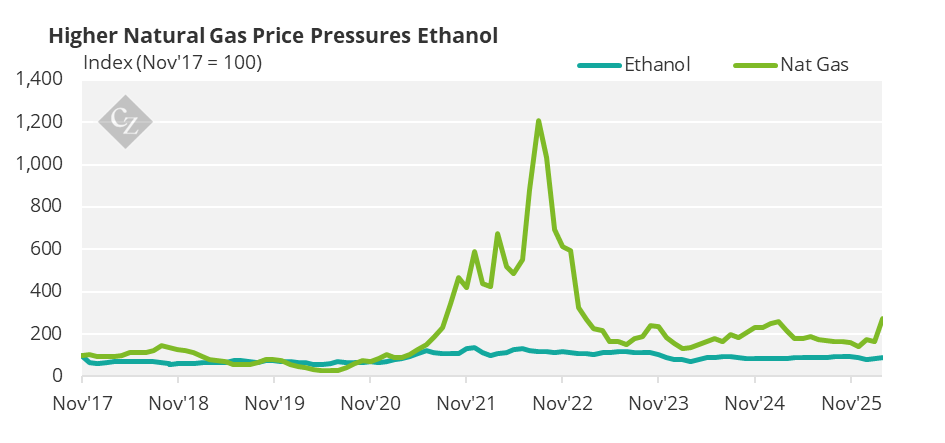

3. Energy Inputs Tie Ethanol Production Costs to Oil and Gas Markets

Ethanol plants consume significant energy (primarily natural gas) for distillation. Higher energy prices (often correlated with crude oil markets) raise ethanol production costs.

4. Government Policy Moderates the Oil–Ethanol Link

Mandates such as the US Renewable Fuel Standard (RFS) require a fixed volume of ethanol blending regardless of gasoline price. These policies underpin structural demand for ethanol, maintaining baseline price support even when oil prices fall, thereby weakening the direct correlation between the two markets.

Corn ethanol pricing does respond to oil prices, primarily through gasoline demand and production‑cost linkages. However, unlike petroleum fuels, ethanol is also anchored to agricultural markets and government policy, creating frequent divergence from crude‑oil trends.

Arbitrage Opportunities for Corn Ethanol

Arbitrage opportunities between corn and corn ethanol arise from price discrepancies across the supply chain connecting raw grain to refined fuel. The most fundamental variable is the crush spread, often called the corn‑to‑ethanol spread. This represents the margin between the market value of ethanol (and its co‑products) and the cost of the corn required to produce it. Since one bushel of corn yields roughly 2.8 gallons of ethanol, plus distillers’ grains (DDGS) and corn oil, any widening or narrowing of the crush spread directly affects arbitrage potential.

Input prices are another major determinant. The cost of corn itself fluctuates with growing conditions, yields, global demand and agricultural policy. Variations in fertiliser, natural gas, electricity and water costs—essential inputs for ethanol plants—can shift production economics and influence whether converting corn into ethanol is profitable relative to selling the grain outright.

On the output side, ethanol prices are driven by gasoline demand, blending mandates, crude oil prices and refinery economics. Since ethanol is primarily used as a gasoline blendstock, higher oil or gasoline prices generally boost ethanol values, improving the arbitrage spread. The value of DDGS and corn oil also matters; strong feed demand or export markets for DDGS can significantly enhance overall returns.

Regulatory factors play an outsized role. The US Renewable Fuel Standard (RFS) and the associated RIN (Renewable Identification Number) prices can meaningfully increase the effective value of ethanol. Changes in policy, obligations or political sentiment can therefore create or erase arbitrage opportunities quickly.

Finally, logistics and regional basis levels (including transportation costs, storage capacity and local supply‑demand imbalances) shape the feasibility of exploiting price spreads. Even if paper arbitrage looks attractive, bottlenecks in rail, trucking or storage can constrain real‑world execution.

Together, these variables determine whether converting corn to ethanol yields a positive margin or whether selling corn directly is the superior economic choice.