Opinions Focus

- A year of extremes in 2022, assessing the impacts on supply.

- The World’s largest wheat exporter is Russia, a country embroiled in war.

- Record heat and lack of rainfall has beset many producing regions.

Introduction

News headlines have exposed the difficulties facing the world’s wheat supply thus far in 2022.

Russia’s war in the Ukraine has been the focus as disruptions to Black Sea shipping has caused major turmoil for many of the big importers, such as Egypt and their fellow North African nations.

With wheat harvests in the Northern Hemisphere moving to the latter stages, forecasts are gaining validity.

Questions remain as to prospects for the Southern Hemisphere harvests and whether global recession fears or extreme weather may yet complicate the historically robust supply chain.

Global Supply and Demand for 2022/23

The news coverage over recent weeks and months with regards record heatwaves, wild fires and drought can create a sense of anxiety over where the World’s food supply will be sourced.

Looking at the estimates produced in the monthly United States Department of Agriculture (USDA) World Agricultural Supply and Demand Estimates (WASDE) on 12th August we can consider the potential impacts over the coming year.

World Production and Stocks

Wheat crops around the World have suffered during the growing season of 2022 as weather records have been broken across the planet.

In spite of these, it is reassuring that the USDA foresee an increase in production year on year.

Year end stocks are more of a talking point as the figure projected for the end of 2023 will be the lowest in six years.

(Estimates in million metric tonnes/mmt)

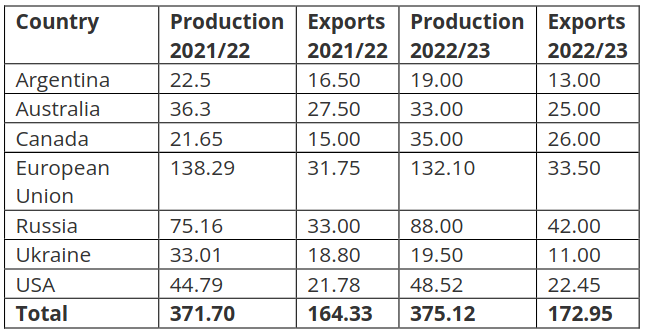

The Major Exporters

(Estimates in million metric tonnes/mmt)

The war in Ukraine will inevitably deplete the country’s 2022 harvest, as seen in the table above. However, supply from the major exporters as a whole, looks fairly stable from a year ago, up 3.45mmt at 375.12mmt.

A reduction in the size of the European Union harvest, plus the significant reduction in Ukraine; is compensated for by the potential for a record crop in Russia and higher production in the US.

Argentina and Australia are still a few months away from harvest, towards the end of the calendar year, but estimates show a slightly reduced level from 2021 and hence lower export expectations.

Despite an increase the situation for the exports looks relatively stable for the year ahead.

China and India

(Estimates in million metric tonnes/mmt)

As the two most populous countries, China and India are influential in any global supply evaluation.

News from China has shown an extraordinary year of heat, drought and high temperatures. With that in mind it will be important for the USDA estimate of 138mmt of production to be realised, thanks to a higher acreage of plantings.

Earlier in the year India had been expecting a huge record crop, but adverse weather has reduced it from the 110mmt some had anticipated, down to the predicted 103mmt.

The Year Ahead and Harvest 2023

As we see combines begin the return to their winter barns, discussions turn to the prospects and sowings for the next 2023 harvest. The Northern Hemisphere will see these underway in earnest over the coming weeks and months.

The weather stories of 2022 will not abate as the autumn drilling campaign progresses. Enough rain to allow large plantings would be welcome as the current high prices will see ample returns to the arable growers.

The outlook should therefore, with a helping hand from the rain gods, see a continuation of the upward trend in World production in 2023 and a hope for increasing end stocks.

Conclusions

The turbulent year of 2022 is heading into its latter months, where war and weather have thrown many of the original New Year thoughts to the winds.

Despite the troubles, production appears to have remained robust, even though end stocks are dwindling.

Acres for the 2023 harvest may well be large, which will aim to rebuild confidence in the longer-term stocks.

Although Russia’s war in Ukraine has had a devastating cost in human suffering, hopefully the recent improvements in Black Sea shipping will continue to ease logistical issues.

There is much reason for optimism as we look to the future of wheat production and overall Global supply.

Confidence in the 2023 harvest wheat supply and more stable logistics could well be the catalyst for calmer markets as we head towards the end of an extraordinary 2022.