Insight Focus

The wider grains complex was pulled higher by a rally in wheat this week due to a reduction in production forecasts and reports of worse than expected quality. Corn markets remain well supplied.

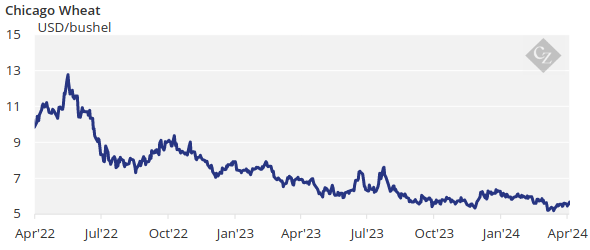

Wheat rallied on the back of worsening conditions in both the US and Europe and pulled the whole grains complex higher. The upside risk we mentioned last week came all at once and now a potential reduction in wheat production both in the US and in Europe should be priced in.

We will have to wait for the May WASDE report to see if it accounts for the production loss. The wheat condition reports this week will probably dictate price action, which should be neutral or negative for prices. No surprises are expected in corn but there is potential for delayed planting in Europe due to excess rains.

There is no change to our Chicago corn forecast for the 23/24 (September/August) crop to average in a range of USD 4.15/bushel to USD 4.40/bushel with an upside bias. The average price since September 1 is running at USD 4.55/bushel.

Wheat Rallies on Negative Data

Wheat started strong last week, pulling the rest of the grains complex higher as the US area under drought conditions increased, crop conditions worsened, and concerns arose about the risk of late frost in Europe. The much worse than expected crop condition in the US further fuel the rally through mid-week.

The rally occurred despite Russia increasing its grain — mainly wheat — export quota by a sizable 5 million tonnes through June 30.

The MARS bulletin from the European Commission confirmed 5% lower yields in the UK and Ireland due to excess rains, flooding damage in some areas of France, Germany, Belgium and Netherlands. While yields are down by 4% year on year in France, the other three countries have not yet reported a reduction in yields. The European Commission also reduced its wheat production forecast by 570,000 tonnes due to lower production in France and Germany.

Source: European Commission

US wheat condition was 50% good or excellent, a sizable five points lower week on week and compared with 24% last year. Areas under drought condition have moved from 18% two weeks ago to 30% last week.

There was noise last week about potential lower Russian production due to dry weather in the south of Russia, but local analysts did not report any big cuts. The French wheat condition was 63% good or excellent, down 1 point week on week and compared with 94% last year.

Corn Pulls Up but Supply Remains Plentiful

Corn had to follow wheat but was also accompanied by US export inspections rallying 20% week on week last Monday. The only negative piece of information came with the weekly planting report showing a big weekly jump in planting progress compared with expectations of much milder advance due to rains in the corn belt. But the pull from wheat was stronger than the planting data.

US corn is 12% planted, up from 6% the previous week and on par with 12% last year. The five-year average is 10%. In Brazil, the first corn crop is 56.7% harvested versus 59.6% last year, and Safrinha corn (the second and bigger crop) planting is now officially finished. In Argentina, the corn crop is 19.8% harvested. Conditions worsened three points to 17% good or excellent.

Russian corn is 25.8% planted, significantly up from 16.3% the previous week. Ukrainian corn planting continued to make huge weekly progress and is now 30% completed — a sizable increase on just 3% two weeks ago.

The MARS bulletin from the European Commission mentioned delays in corn planting due to excess rains. The European Commission left its corn production forecast unchanged at 62.2 million tonnes.

Source: European Commission

The US is expected to receive good rains across the corn belt and the wheat areas. US corn area under drought conditions was unchanged at 23% while wheat area worsened a sizable 6 points in the week to reach 30%.

Brazil is expected to be dry in most areas except in the south, and Argentina is forecast to receive good rains across all agricultural areas. Dry weather is expected in central Europe while France should continue to receive rains.