Insight Focus

- What is the Cash-and-Carry trade?

- We work through an example using butter.

- Risks and opportunity of this type of structure.

This article will be the first in a series which sets out to unpick several dairy trading strategies. These strategies will be across physical and financial markets, sometimes utilizing both.

After my last piece in which I mentioned that “European traders are facing challenges in executing the Cash-and-Carry trade for butter as reefer warehousing space is increasingly hard to access” I received several messages asking what exactly that meant. I thought it would be good for the focus of my next piece, and the first of this series, to be on the “Cash-and-Carry trade” topic.

Definition of arbitrage: the simultaneous buying and selling of securities, currency, or commodities in different markets or in derivative forms in order to take advantage of differing prices for the same asset.

What is a Cash-and-Carry Trade?

- Simply put, when it is cheaper to buy a product for delivery now and hold it for several months than to buy that same product for delivery in several months there is an opportunity for a Cash-and-Carry trade.

- If this opportunity were present, a trader would seek to profit from this by buying, storing and funding the goods for “x” months, while simultaneously selling the associated futures contract for “x” months’ time. It is an arbitrage trade.

Example of how to structure a typical Cash-and-Carry Trade:

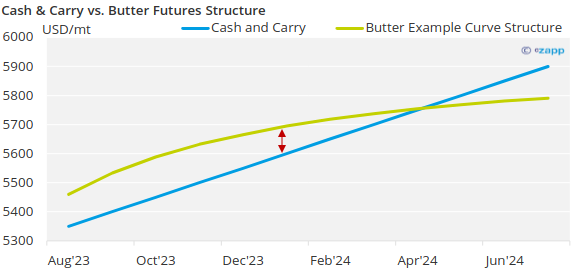

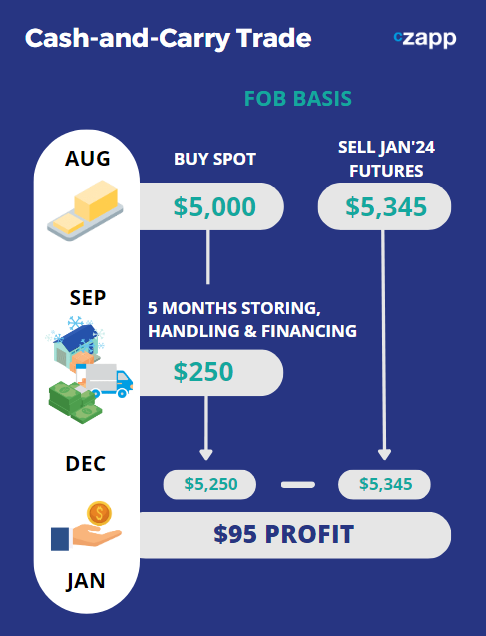

- Let’s say that you are based in Singapore and Unsalted Butter is currently being offered to you for spot delivery to your warehouse in Singapore at $5,350 USD/MT (basis $5,000 USD/MT FOB pricing).

- You don’t actually need any butter until January 2024 though.

- The NZX-SGX futures are offering butter for January arrival at $5,345 USD/MT FOB which works out to $5,695 USD/MT delivered to your warehouse in Singapore. Producers are offering physical butter for January 2024 arrival at prices higher than this, so the futures are the better value long tenor offer.

- Your other alternative is to buy the butter now and store it until you need it in January. “Spot” in this sense means August arrival. So you will have to store the butter for five months and assuming that you are buying it on cash terms, you will have to finance it for five months too. If the cost of refrigerated storage, haulage to the warehouse and handling charges while there plus your financing for five months sum to $250 USD/MT then the total cost of butter in January through this mechanism is $5,600 USD/MT.

- So, the trader would buy spot butter for $5,000 FOB and simultaneously sell the associated futures at $5,345. They would book prompt sea freight at $350 which would be required regardless of whether they had bought butter prompt or longer tenor. They would also lock in the cost of handling, storage and finance for this butter for five months for $250.

- Given that freight is required regardless, the comparison is then $5,345 vs. $5,000+$250, a $95 difference in pricing that the trader has been able to exploit and profit (red arrow in chart above). They have successfully created an arbitrage through structuring a cash-and-carry.

- By buying the physical butter and selling the futures, the trader has likely also helped the market to close a mispricing and be more efficient. I.e. they have tightened the sales book of the seller who can now confidently offer butter at a little higher price. They have also possibly sold through some bids on the derivative market to cover their volume, providing valuable liquidity to the futures market and causing the derivative price to go down.

- To summarise: if the cost of buying a product now in the cash market and carrying it for use in several months is cheaper than the futures offer for the same month, then the market is offering users of that product value. This value can be captured by buying the cheap butter now, carrying it and simultaneously selling it for more in the future.

Inverse Cash-and-Carry Trade?

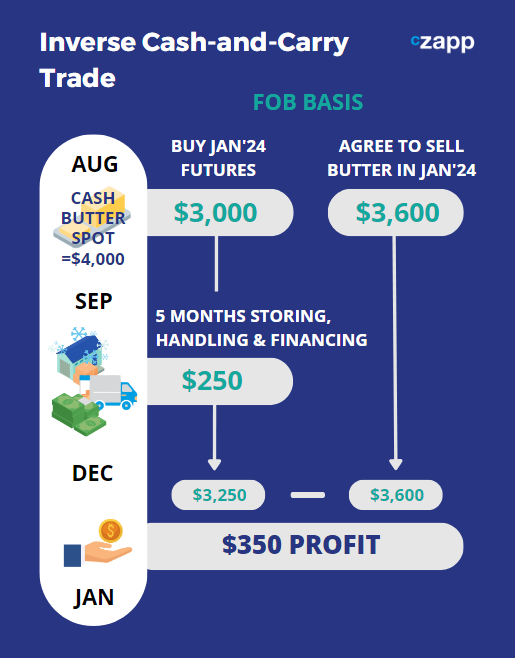

- When the derivatives market is steeply backwardated (i.e. the futures curve is downward sloping) there may be the opportunity to structure the cash-and-carry trade in reverse).

- That being, if the market is willing to buy physical butter for forward delivery at a price premium to the futures market for the same time period, then there is also an arbitrage opportunity.

- A trader can execute this by selling physical butter for delivery in month T and simultaneously buying the butter futures for month T. If the cost of storing, handling and funding this butter from now until month T is less than the difference in the physical sales price and the futures buy price then they have achieved an arbitrage.

- For example, if cash butter is $4,000 USD/MT FOB, the cost of carrying sums to $250 USD/MT for five months, and the futures price for month five is $3,000 USD/MT FOB. Then if the trader can sell butter in month five at say $3,600 and buy the futures for $3,000 then they have locked in a $600 differential and a risk-free profit of $350 ($600-$250) once carrying costs are accounted for.

Risks to be aware of when entering the Cash-and-Carry Trade:

- “Getting out” is the biggest risk and can present a challenge. In the typical cash-and-carry the buyer is long physical and short a derivative. To execute this properly the trader needs to be able to:

- Sell the physical at a market price at their chosen time horizon. There is inherent risk in that they must find a willing buyer.

- Buy back the derivative contract (unless they are holding this to settlement). If they are buying it back then there is derivative liquidity risk. I.e. there may not be sufficient amounts of offers in the market to exit the derivative, or doing so may come at an unattractive price.

- Basis risk on the derivative: the derivative instrument must be well correlated to the physical market pricing of the product. If it is not, then risk is added if the derivative pricing diverges from the physical product pricing over the duration of the trade.

- Warehousing risk: a food grade warehouse which is approved for this product and in a suitable location must have space available for your goods to be stored at. If the local warehousing is all full then this can impact the ability to enter this structure even if the numbers seem to make sense.

- Physical supply chain and quality risk: the goods must be moved and stored correctly so that they are still of saleable quality at the end of the trade. This can be mitigated through insurance to a large degree. Goods must also be handled within their correct shelf-life and traders must be aware of any market restrictions on shelf-life at time of import etc. as well.

- Interest rate risk: the financing cost can change while the goods are in storage, this can materially increase the cost of carrying. This can be mitigated by using interest rate derivatives to lock in any floating component of the financing rate.

Want to be able to do this when the market gives you the opportunity but can’t? Call us!

- To construct a cash-and-carry on your own you need:

- Access to physical product.

- Access to the associated/appropriate derivatives market.

- Warehousing and logistics capability, including cold-chain for reefer goods such as butter.

- The ability to fund large value flows for several months.

- If you think that this kind of structure could benefit your business but don’t have all of the components in-house, then CZ can help facilitate this for you transparently.

- Get in touch with Tom at TSoutter@czarnikow.com.