Opinions Focus

- The USDA forecasts lower wheat demand in 2022/23.

- This is partly due to volatile wheat prices coupled with rising costs.

- Global recession forecasts may well influence demand.

Introduction

War and weather have been the major news headlines surrounding the wheat markets during 2022. However, these have focused mainly on the impact of supply, only one half of the story.

Looking more specifically at the demand side of the market may help to assess possible repercussions heading towards the last quarter of 2022.

World Production and Demand

Examining the United States Department of Agriculture’s (USDA) September World Agricultural Supply and Demand Estimates (WASDE) report, there are some interesting numbers concerning global demand for 2022/23.

The estimated demand worldwide for wheat climbed 8mmt from 2020/21 to 2021/22. However, despite the global population forecast climbing to surpass 8 billion in November 2022, according to the United Nations, there is likely to be a marginal reduction in wheat demand in the current marketing year.

Needs of the Importers

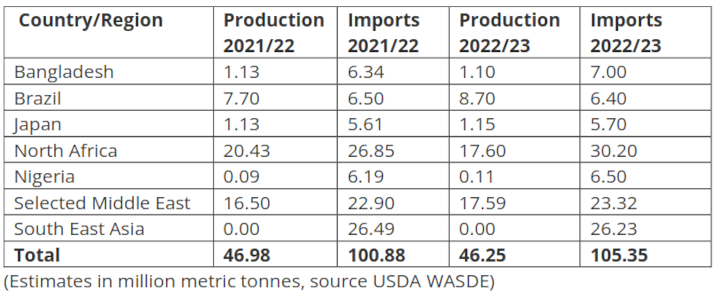

Although demand is anticipated to drop during the year, that is not all good news for the poorer countries of the World’s largest importing region of North Africa.

Due to the much-publicised extreme weather worldwide, North African production has suffered and crops are smaller, resulting in increased import projections.

China and India

As the two largest producing and consuming countries of the World, estimates for China and India in 2022/23 are of significance.

Interestingly India has the potential to overtake China as the most populous country during 2023, while their wheat usage remains considerably lower than that of China.

Weather has detrimentally impacted wheat harvests for both countries, with India expected to see a drop in production.

Demand in both countries is forecast to decline in the current year, with a combined drop of nearly 10mmt.

The Year Ahead

As numbers in the tables above suggest, overall demand should be a little lower than the preceding year.

News headlines foreseeing recessions and a tough winter ahead for large swathes of the Global population are certainly impacting demand.

High fuel and energy prices coupled with inflation and rising interest rates have potential to diminish funds available for anything other than the bare essential foods for many millions around the World.

Conclusions

War and weather have played significant roles in huge volatility in the wheat prices throughout 2022.

Populations are growing as we surpass 8 billion people on Earth, with many concerned about finances.

People need to eat, but with the exception of the World’s poorest, savings can often be made when finances are stretched.

As economies struggle and people look to reduce their outgoings wherever possible, it is no wonder wheat demand is predicted to shrink. A trend that may well continue over the coming months.