- Diminishing world stocks, war, heatwaves and global economic turmoil make 2022 unique.

- Supply uncertainty remains despite Ukrainian ports restarting exports.

- Drought in Europe causes inconsistent wheat production forecasts.

A unique year, the story so far

In the latter months of 2021 wheat prices rose as world stocks dwindled and the outlook remained uncertain as 2022 began.

At the end of February, Russia invaded Ukraine, and prices skyrocketed to unprecedented levels on world wheat markets.

In mid-May there was a cooling off, with prices tumbling. Driven down by renewed hopes for 2022 production, coupled with optimism that the effects of Russia’s war in Ukraine would begin to ease. Exports from the Black Sea might again be able to help feed the import dependent North African nations and enthusiasm for a calmer market place.

Europe has suffered heatwaves in recent months, smashing all-time temperature records. Estimates of both quantity and quality of the rapidly advancing Northern Hemisphere harvests are looking extraordinarily inconsistent.

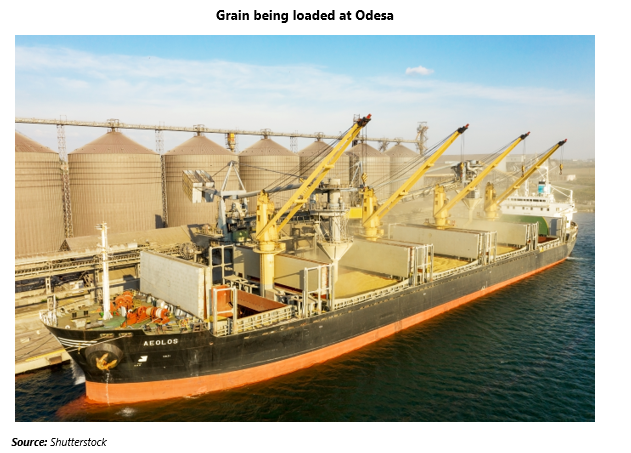

Some more positive news in the last few days sees vessels loaded with grains leaving Ukraine’s Black Sea ports destined for Europe, North Africa and Asia.

Global banking systems are raising interest rates as economies endure inflation and recession with the fallout from both the war in Ukraine and the continued fight against COVID, most notably in China.

Sources of Uncertainty

Ukraine and Black Sea exports

As news headlines report loaded ships leaving Ukrainian ports, the sustaining and volume of exports is an unknown.

Large tonnages will require a continued joint effort from both Russia and Ukraine, fortunately aided by Turkey and the UN.

Ukraine’s devastated infrastructure will no doubt struggle if, as we hope, volumes carry on being laden onto boats.

Production estimates

With war still raging, Ukraine’s 2022 wheat harvest is hard to predict at best. The harvest to date is reported to amount to just over 12.6m tonnes, but whether the final figure will be more or less than the predicted 20m tonnes remains highly debatable.

Russia has repeatedly predicted a large crop, up from 75m tonnes last year. In the last week IKAR has suggested a huge 95m tonnes while the Russian Agriculture Ministry has begun to suggest that weather and a lack of machinery parts may lead to a reduction in forecasts from their previous estimate of 87m tonnes.

France is completing its wheat harvest, where the Agriculture Ministry is estimating a crop of 33.87m tonnes of soft wheat, up from last month’s forecast of 32.9m.

Germany’s DBV estimates winter wheat production was 1% higher year on year, at 21.38m tonnes as harvest nears completion.

The US wheat crop has potential to be enhanced by the spring wheat harvest resulting in a 2% month-on-month increase to 48.6m tonnes.

Argentina’s recently planted crop has received much needed rain, but dryness persists and production forecasts may well be cut further.

Global economy

Brent crude oil is heading down towards the low USD 90s a barrel, levels not hit since March.

Inflation and interest rate rises are exercising economists worldwide.

The zero-COVID policy and lockdowns in China look set to reduce its economic outlook.

US Speaker Nancy Pelosi’s visit to Taiwan last week enraged the Chinese government, prompting large-scale military drills near the island. Any further geo-political tensions could fuel fresh market turbulence.

Estimates for 2022 world production and hence year-end stocks, are unlikely to stimulate much confidence for months to come.

Global economic woes may dampen the enthusiasm for any significant wheat rallies.

Conversely heightened geo-political tensions could prompt significant market disruption.

The current high wheat prices will very probably, weather permitting, lead to large plantings in the coming months for the 2023 harvests.

The possibility of increased production in 2023 should cap any price rallies. However, although we hope for some peace in Ukraine and calmer wheat markets as 2022 moves on, a watchful eye on geo-political turbulence is advised.

Other Insights that may be of interest

What the Energy Crisis Means for Inflation & Commodities

Interactive Data Reports that may be of interest …

Consecana Panel