Opinions Focus

- Wheat volumes from the major exporters are lower year on year.

- Russia considers removing wheat export quotas with a record crop.

- Demand erosion may be demonstrating problems for buyers.

Introduction

Economists tell us that supply and demand drive price.

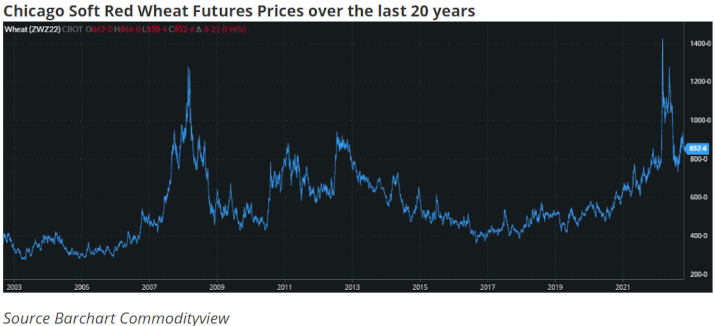

Wheat values around the globe are some way off the record highs seen earlier this year. Nonetheless, prices are high in historical terms.

The possibility of reduced demand, in a perfect market, is therefore likely.

Wheat is not a perfect market and people need wheat to eat and survive.

Disruption caused by Russia’s war in Ukraine has impacted fuel and energy costs to much of the World’s population.

Assessing wheat demand over the coming months, as a result of these increased costs, presents some intriguing questions.

Export progress

The Northern Hemisphere winter wheat harvest is all but finished, with spring wheat harvests rolling on in parts.

With the major exporters in this region, Russia, Europe, the United States and Canada; export progress is important at this time of year.

Cumulative exports from these big exporting nations is falling short of expectations and in parts lower than any of the previous 3 years.

Importers Costs Rising

The largest importing region of the World is North Africa where wheat is a vital food staple for the populations. These are also some of the less wealthy nations.

With increased fuel and energy values the cost of wheat imports is staggeringly high when coupled with the wheat prices seen in the charts above.

With current prices the financial implications to nations such as Egypt, the World’s largest buyer, subsidising the price of wheat to the people creates real concern.

It is therefore of little surprise that purchases are more on a short-term need basis, rather than forward purchasing for longer term food stability.

Russia’s Actions

As the largest exporter, engaged in a costly war, with a record harvest, Russia’s actions over the coming weeks and months will be closely watched.

The Black Sea grain corridor, allowing grain exports from the Ukraine is in jeopardy.

Brokered by Turkey and the United Nations, Ukraine and Russia have an agreed system to allow exports from Ukrainian territory.

In one month, it comes to an end.

Russia is threatening any extension unless certain criteria are met. These relate to who can receive the grains, together with agreement on grain and fertiliser exports from Russia.

However, the need for sales has prompted the Russian government to recently suggest that the current grain export quotas will be lifted, with a view to encouraging greater sales volumes.

Suggestions from the Russian government that they may help certain countries finance imports of Russian wheat, could also help alleviate some of the pain for importers.

Conclusions

Demand is undoubtedly being affected by high costs, both in terms of the basic wheat prices and high shipping costs associated with high fuel and energy values.

Importers have financing concerns, while weighing these up against a backdrop of potential unrest among their populations if food security is not preserved.

Russia needs money as well as to empty the bulging stores of wheat across the country.

With a war far from going according to plan, Russia’s President Putin may use any method at his disposal to apply pressure to the outside world.

It is hard not to see President Putin use wheat as leverage in his political struggle with the West, which may well cause a price spike if agreement is not reached for the Black Sea grain corridor next month.

The Russian’s need for sales together with the importing nations need for food, may well be the necessary ingredients to maintain supply to the market while high prices keep demand in check.

Price rallies in the coming weeks and months are almost inevitable, but demand is likely to be scared away keeping them short-term. While market drops will see the buyers reappear with enthusiasm.