Insight Focus

Grain markets rallied on supportive USDA data. Below-expected US corn and wheat stocks, combined with hot weather across Europe, supported prices, although European wheat came under harvest pressure and French crop conditions deteriorated sharply. Attention now turns to this week’s WASDE report, with volatility likely as traders weigh potential upside to US corn yields against a likely downgrade to French corn production.

This update is from Nixal Commodities. For more information, CLICK HERE.

Grains rallied on a supportive USDA acreage and stocks report, as well as continued hot weather in Europe. European wheat fell under harvest pressure, while French crop conditions plummeted.

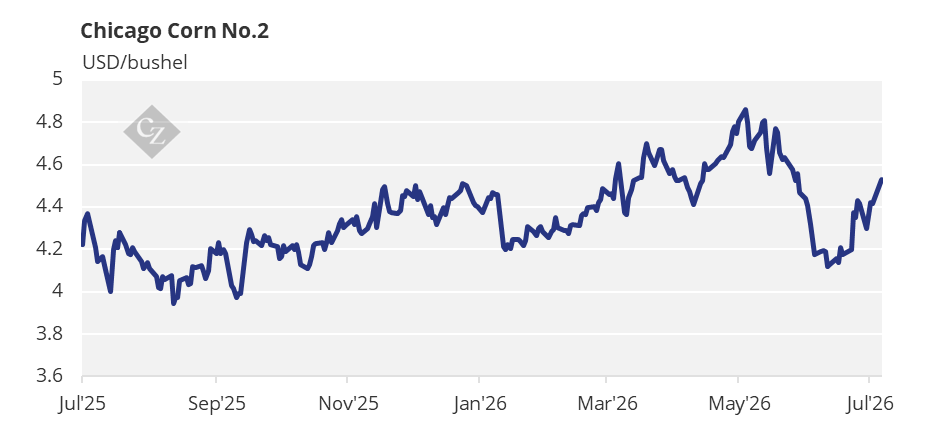

Corn in Chicago has now moved away from the USD 4/bushel region after corn acreage remained unchanged, eliminating the risk of higher acreage that would have justified a sub-USD 4/bushel market. However, the market’s focus now turns to the July WASDE, due this Friday, with corn yield the key variable that could move prices.

The last WASDE showed a yield of 183 bushels/acre, down from 186.5 bushels/acre last year and therefore below trend. However, weather conditions have been favourable and fertiliser availability should no longer be an issue, so there is a chance of seeing higher yields in the upcoming WASDE, which would be bearish for the market.

On the supportive side, the impact of the French heatwave on corn yields still needs to be assessed, and last week’s 18-point decline in corn condition is not an encouraging signal.

With the market focused on the July WASDE this week, expect another volatile week. We believe there is a risk of higher corn yields, implying downside risk for Chicago prices, while a downward revision to French corn production is also expected.

There is no change to our forecast for Chicago corn to average USD 4.4/bushel during the 2025/26 (September/August) crop.

Supportive Stocks Data and Heat Support Corn Prices

Corn in Chicago opened lower last Monday ahead of the acreage report expected on Tuesday. However, it rallied following the report’s publication on Tuesday and continued to strengthen through the rest of the week, supported by hot weather reaching key corn-growing areas. It ultimately closed the week in positive territory.

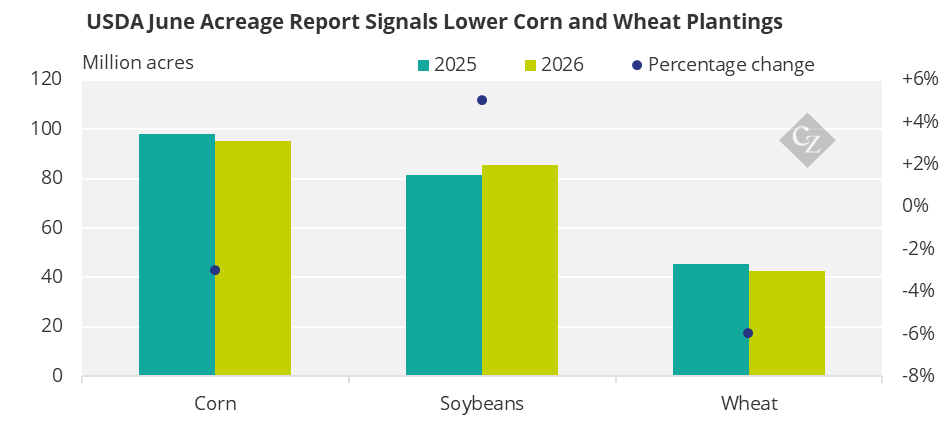

The USDA acreage and quarterly stocks report published last Tuesday was supportive for both corn and wheat.

Source: USDA

Corn planted acreage came in at 95.3 million acres and harvested acreage at 87.4 million acres, unchanged from the June WASDE. The market was expecting a range between 95 and 96 million acres, so coming almost in the middle of that range and unchanged from the June WASDE, this was a non-event for the market. However, US corn stocks as of June 1 were 5.3 billion bushels, significantly up from 4.64 billion bushels last year, but below market expectations of 5.4 billion bushels, which gave a boost to the market following the publication.

On top of the supportive report, a heatwave forecast to last through the weekend and into this week provided additional support to corn in Chicago during the second half of last week.

Trump did not renew the US-Mexico-Canada trade agreement, which formally came up for review on July 1. This decision does not suspend the terms of the agreement, as they remain in force unless any country withdraws with six months’ notice. However, it opens a period of negotiation if the agreement is to be extended beyond 2036.

Moving to Europe, a French growers’ association said corn production could plummet by 30% to a 26-year low, as many farmers were unable to plant. This came alongside the condition report published last Friday, in which corn conditions fell by 18 percentage points.

US corn condition is 67% good or excellent, down one point week-on-week and compared with 73% last year. Corn condition in France is 58% good or excellent, down a massive 18 points week on week versus 78% last year. Corn planting in Russia is complete. Summer corn harvesting in Brazil is 95.3% complete versus 95.4% last year and the five-year average of 94.9%. Safrinha harvesting is 18.8% complete versus 17% last year and the five-year average of 24.6%. Corn harvesting in Argentina is 52.9% complete.

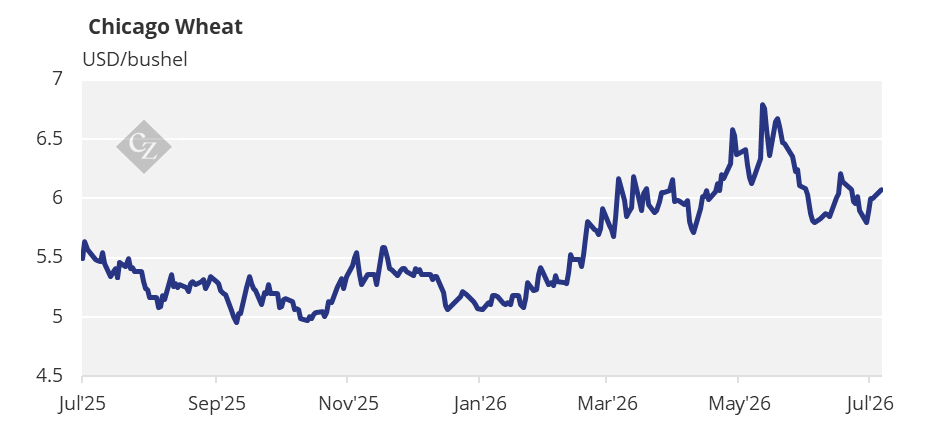

Bullish USDA Data Lifts Wheat

Wheat came under harvest pressure and posted a small decline in Europe despite further deterioration in French wheat conditions. However, Chicago wheat rallied on the back of the supportive US acreage and quarterly stocks report.

US wheat acreage came in at 42.7 million acres, down from 43.8 million acres in the June WASDE and lower than market expectations of almost 44 million acres. In addition, US wheat stocks as of June 1 came in at 920 million bushels, significantly up from 855 million bushels last year but below market expectations of 934 million bushels, which helped support a positive week.

US winter wheat is 48% harvested versus 34% last year and the five-year average of 39%. Condition is 26% good or excellent, unchanged week-on-week and compared with 48% last year. US spring wheat condition is 59% good or excellent, up three points week-on-week and compared with 53% last year.

French wheat is 68% good or excellent, down eight points week-on-week versus 76% last year, while harvesting has started and is 26% complete, up from just 9% last year and the five-year average of 5%. Wheat planting in Brazil is 87.3% complete versus 63.8% last year and the five-year average of 73%.

A cold front is expected to bring cooler temperatures to northwestern Europe, as well as eastern Europe and the Black Sea region, alleviating the heatwave of recent days. However, southern Europe, including France, is forecast to remain very hot.

The US Corn Belt is expected to remain hot but also humid, which should be beneficial for corn development. Little to no rainfall is forecast for Brazil’s Centre-South after several weeks of rain. Argentina is expected to experience very cold and rainy weather.