Watch the on-demand webinar here.

Insight Focus

Brazil’s grain demand is split between exports and domestic use. By 2025, 48% of soybean production went to China, while 70% of corn was consumed domestically. Higher biofuel mandates support demand, yet producers still question why prices are not reacting more strongly amid rising geopolitical tensions.

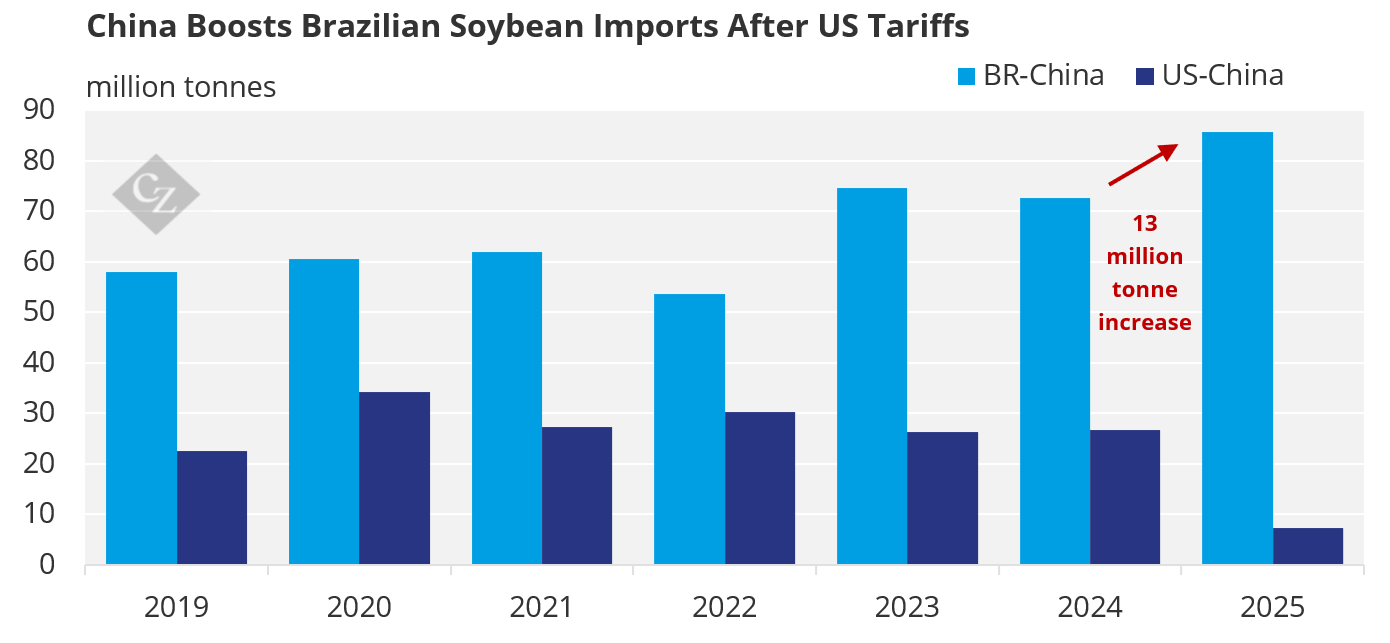

China is still the most important buyer in the global soybean market. Brazil depends on Chinese demand, but after the US tariffs, the Latin American country gained more space in the Chinese market.

By 2025, 48% of Brazilian soybean production was exported to China; that is, 13 million tonnes more Brazilian soybeans going to the Asian country.

Source: USDA

Domestic Demand Anchors Soybeans Beyond Exports

Although exports represent a large market for soybeans, they are not the only one. A large crop can also be absorbed through the crushing industry, which links grain supply to livestock production, vegetable oil demand and biofuel.

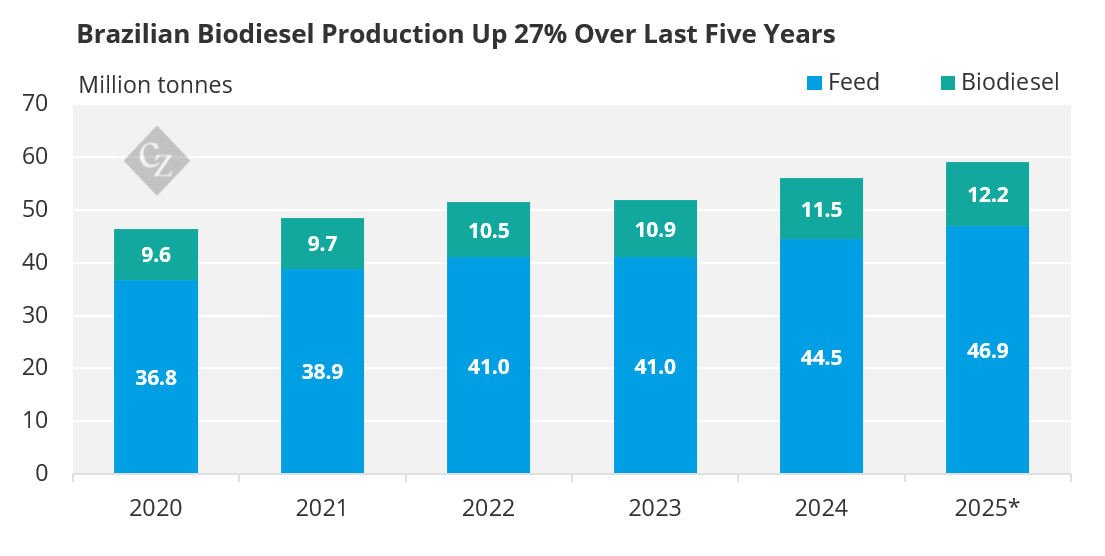

Nearly 30% of Brazilian soybean production is crushed, and almost 80% of soybean crushing is destined for the animal feed market. But another byproduct has been supporting domestic processing and gives the market an additional demand anchor beyond exports.

In 2025, the government increased the biodiesel mandate to 15%. Rumours suggest there may be a further increase to 17% in 2026 due to cost pressures from high Brent crude prices.

Source: Conab

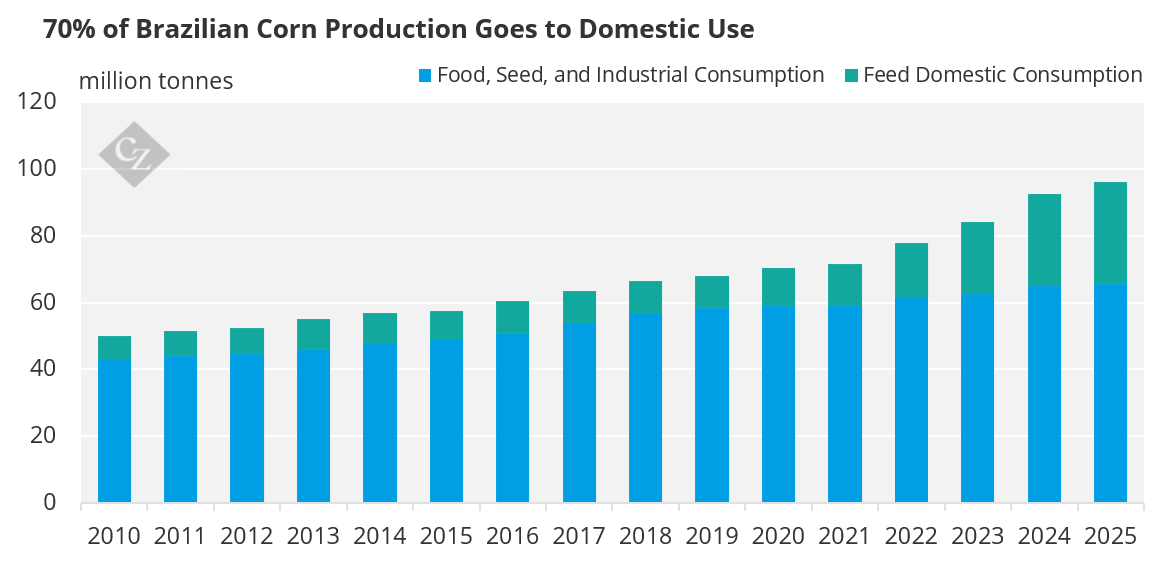

More than 70% of Brazilian corn production goes to domestic consumption, making corn structurally less dependent on export demand than soybeans.

Domestic absorption comes from feed, food, seed, industrial use and ethanol production. While soybeans and corn compete for the animal feed market, corn has also found support in the growing use of biofuels. In 2025, the Brazilian government increased the ethanol blend to 30%, and there are ongoing discussions to raise it to 32% in 2026.

Source: USDA

Although both grains compete for attention in the livestock production market, they do not compete for land. In Brazil, due to soil quality and climate, it is possible to produce up to three crops in the same year.

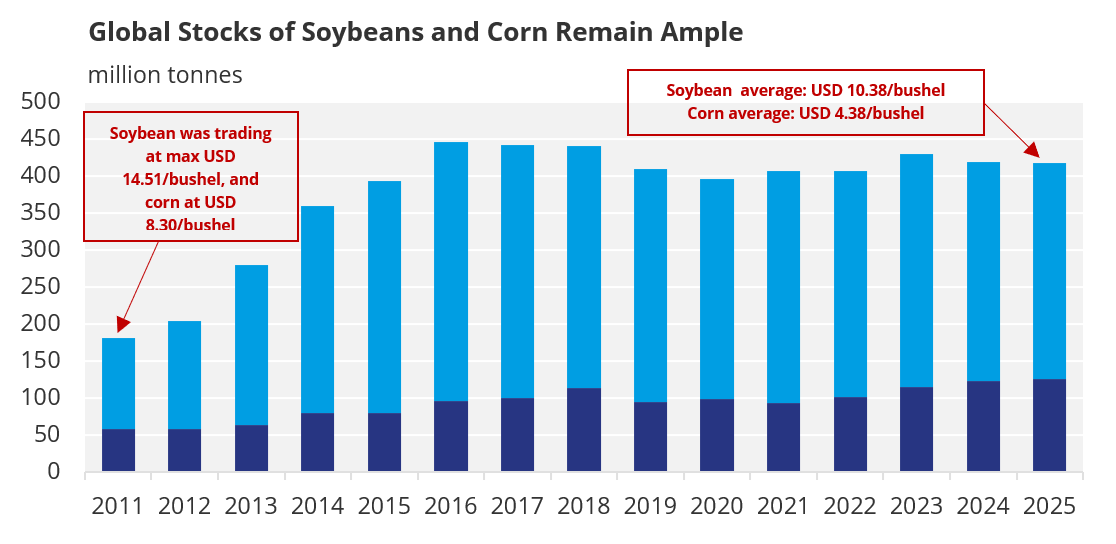

Ample Supply Keeps Prices Under Pressure

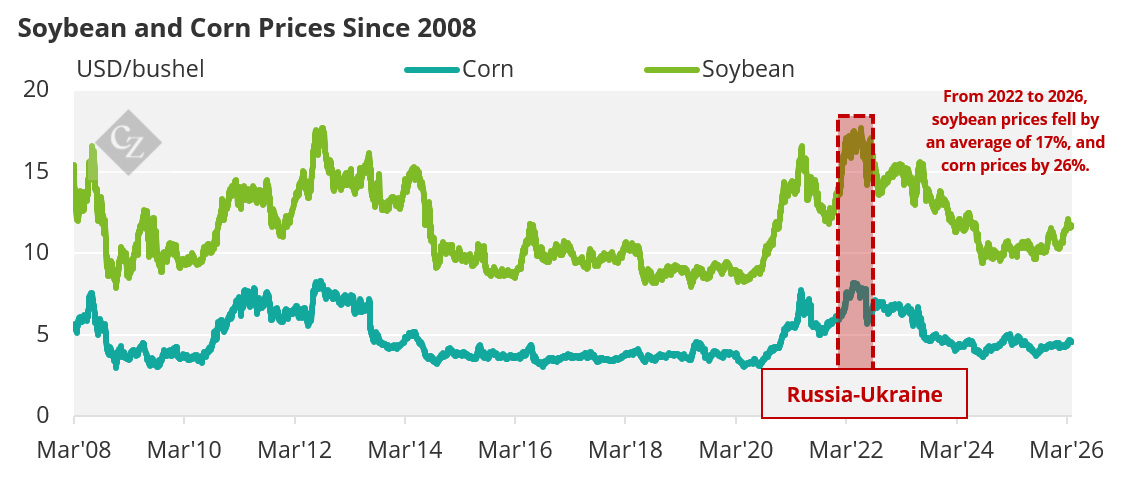

In 2022, energy prices put pressure on global economies due to the Russia–Ukraine war. In 2026, we are once again seeing a similar situation with the US–Israel–Iran war. But the difference lies in the timing. In the first conflict in 2022, the logistical risks resided in the Black Sea, responsible for the flow of 70% of Russia’s grain exports. The market perceived a supply risk.

The 2026 conflict has directly impacted the energy sector. The Hormuz blockade affects the global supply of oil and fertilisers, which are also important for grain production. However, Brazil is currently finishing a large soybean crop of 180 million tonnes, and estimates point to a large corn crop this year as well. Prices for both grains are pressured by large global supplies.

Source: CBOT

Even with fertiliser prices rising significantly, the market is priced in for the large Brazilian and US crops. The risks of lower production in both countries due to increased production costs—energy, freight and fertilisers—are not yet being priced into futures.

The market is still waiting to see how the US corn crop, which is currently being planted, will perform, and for new projections when the next Brazilian crop starts to be planned. Currently, comfortable global stocks of soybeans and corn are holding back a larger increase in prices.

Source: USDA