Insight Focus

Three major SMP demand outlets – Brazil, Mexico and Southeast Asia – may be opening for Europe at the same time, just as US and NZ powders look relatively expensive in different ways. Global dairy markets remain broadly supported, but the more important shift is structural. The market is therefore less about current supply and more about where incremental demand flows next, particularly under rising El Niño risk.

Super El Niño Moves to Centre Stage

The past month’s dairy market has looked firm on the surface, but the more important development is what may come next. A possible Super El Niño is starting to shape how participants think about powders, trade flows and import risk.

Dairy does not react to El Niño in the same immediate way as soft commodities like sugar, but the mechanism is well understood: pasture stress and water constraints typically emerge first in Latin America and parts of Asia, before translating into higher import requirements several months later.

Early signals are already forming. Brazil’s dairy imports are rising, with Jan–Apr WMP up 8.05% and SMP up 6.95% (CLAL), suggesting the market is beginning to position ahead of potential weather disruption rather than reacting after the fact. Brazil could become a larger WMP importer and potentially a meaningful SMP buyer. India also sits in the background as a potential swing importer if monsoon performance weakens.

This forward weather risk is now colliding with a market that, for now, still has rising milk output across major exporters. The result is a disconnect between comfortable current supply and a much more uncertain forward demand map.

Source: NZX

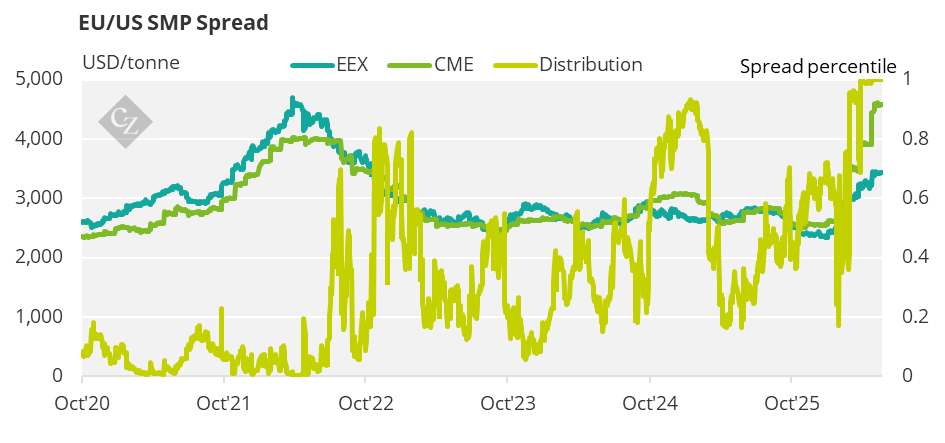

SMP Spreads Point to Europe

The clearest structural story in dairy currently sits in SMP. Relative pricing has opened a rare arbitrage window where European product is now the most competitive origin into multiple major importing regions at once. Western Europe SMP continued to strengthen in May, with USDA and CLAL quoting USD 3,300–3,625/tonne on May 22, but Europe still appears cheaper than the US on a relative basis.

US NFDM/SMP is extremely expensive relative to other markets, sitting at the top end of its historical spread to European product. At the same time, North African tenders have been clearing at materially discounted levels near USD 3,000/tonne pre-GDT, with similarly cheap offers from other non-mainstream origins highlighting just how elevated mainstream US pricing has become.

This creates an unusual alignment: three large demand centres—Brazil, Mexico and Southeast Asia—are simultaneously positioned to increase reliance on European SMP.

Mexico remains structurally tied to US supply, but current pricing makes substitution increasingly attractive. Southeast Asia, meanwhile, is the most price-sensitive region and the most likely to shift volumes quickly, particularly if NZ SMP struggles to hold its premium as new season production begins to build.

The result is that Europe is currently the only origin competitively positioned across all three regions at once.

Trade Flows Are Shifting

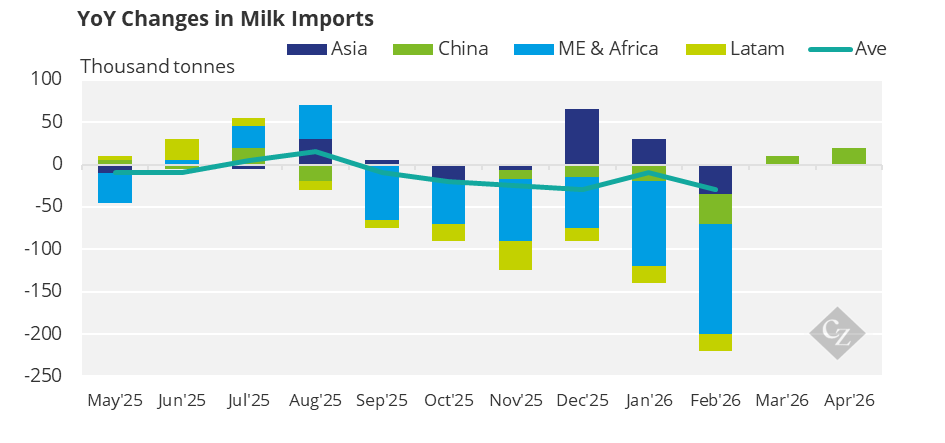

Recent trade flow data broadly reinforces the idea that incremental demand is shifting away from China and toward price-sensitive importing regions.

Trade flows through May reinforced that theme. Fonterra’s May global dairy update showed New Zealand dairy exports up 16.3% year on year in April, driven by WMP and SMP, with exports to China up 18.8%, including a 58.3% jump in WMP shipments to China.

China’s total dairy imports in April were also up 10.2% year on year, mainly because of stronger WMP arrivals from New Zealand. That suggests China is not absent; rather, it is participating selectively and at moments that fit its inventory needs.

Source: NZX

But the bigger structural demand story still sits outside China. USDEC data show global dairy trade up 1.1% year on year in January, with Southeast Asia up 10% and MENA up 14%, while China/HK fell 11%. In NFDM/SMP specifically, Southeast Asia demand rose 13% and MENA demand 51%.

On GDT this week, SEA was the largest buying region for WMP for the first time since July 2024, and historically that has often signalled perceived value. So, even if outright prices look inflated, the buying pattern implies importers still see strategic value in coverage.

Supply Is Abundant, But Vulnerable

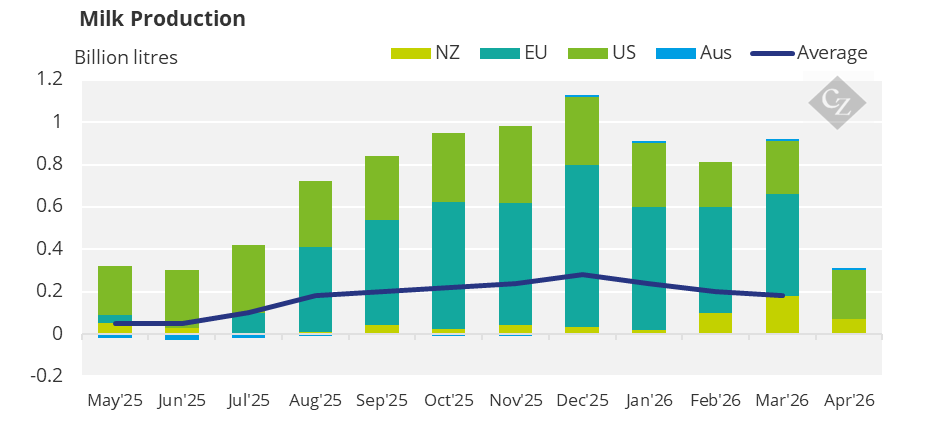

On paper, supply looks comfortable. Fonterra/NZX data show New Zealand milk production up 6.9% in April, Australia up 6.1%, EU up 4.5% in March and US up 3.4% in April. New Zealand collections were 123.6 million kgMS in April, up 7.3% year on year, and season-to-date collections were 4% above last season. That is a broadly bearish milk story.

Source: NZX

Yet the market is not trading as if milk alone determines value, because product mix and weather risk matter more. From July, GDT offer volumes begin to ramp up, and historically higher offer volumes weigh on price.

So, the key question for the second half is whether expanding New Zealand availability can overpower El Niño-inspired import risk.

If a Super El Niño starts to damage pasture, reservoir levels or feed economics in Brazil or India, then today’s “ample supply” narrative could quickly become a story of powder redistribution, not oversupply.

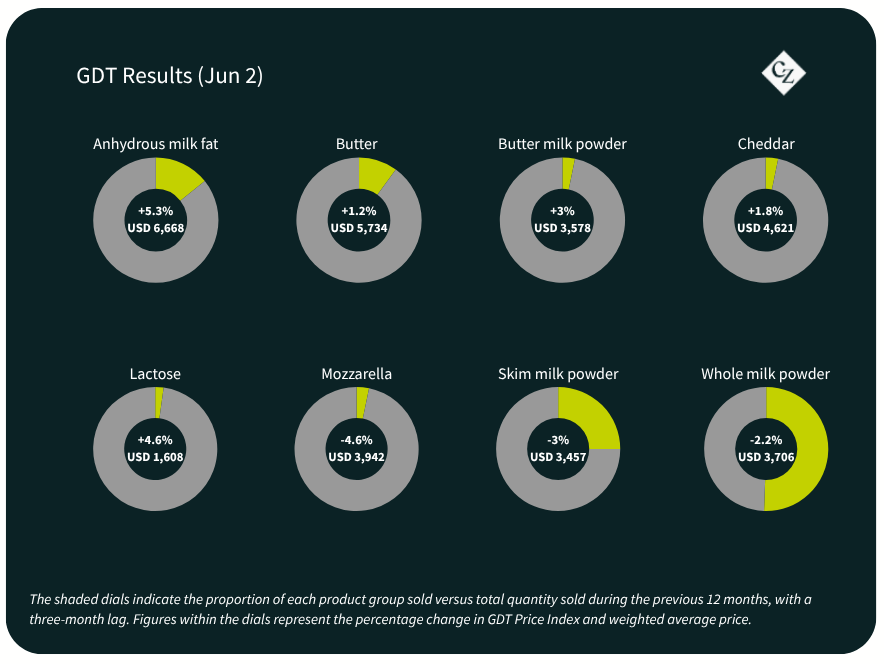

GDT Softens, But Only Selectively

The latest GDT auction on June 2 showed the first meaningful pause after powders had led the market higher through May. The overall GDT index fell by 0.6%, with WMP down 2.2% to USD 3,706/tonne and SMP down 3% to USD 3,457/tonne.

The message is that powders corrected, but fats stayed firm, suggesting the market is rebalancing rather than collapsing. This matters because through most of May, powders had been carrying sentiment. The previous event on May 19 had shown WMP up 1.2% and SMP up 0.2%, while Fonterra’s own auction summary for that event showed WMP and SMP still clearing at historically healthy levels.

The latest softening therefore looks more like a check on aggressive buying than a rejection of dairy fundamentals. That is especially true given that New Zealand sellers are still sold forward several months, despite strong milk production and still-muted narratives around Chinese demand.

The Forward Trade Is El Niño

That is why the most important development of the month is not simply that GDT softened or that milk output rose. It is that the market is beginning to price a weather premium into future powder trade flows.

Europe looks increasingly well-positioned in SMP. New Zealand still dominates WMP, but July volume growth may test that pricing power. And Brazil, Mexico and Southeast Asia look like the three biggest demand pivots, with El Niño potentially adding a fourth in India later on. The key question for the coming weeks is whether El Niño risk begins to translate into earlier-than-expected import demand (particularly from Brazil) just as European SMP sits at a relative discount and NZ enters its higher offer-volume period.

If that convergence occurs, the current arbitrage could close quickly, shifting Europe from a price follower to a price setter in key powder markets.